Key Focus This Week:

“A Phase of Cross-Asset Pricing Converging Toward Core Macroeconomic Variables”

The first major catalyst this week comes from manufacturing data, whose role is more about refining the market’s assessment of the economic cycle than confirming a new trend. Investors will closely examine the interaction between new orders, production activity, and inventory dynamics to determine whether businesses remain in the final stage of destocking or have begun transitioning toward demand stabilization. At the same time, employment components and prices-paid indices will be scrutinized for signs of renewed cost pressures, which could influence assumptions regarding the pace of corporate margin recovery. At this stage, manufacturing data serves as a “low-frequency filter” for cyclical signals, providing the structural framework for interpreting subsequent releases.

Market attention will then shift to services-sector indicators and labor-market-related high-frequency data, which directly reflect the resilience of domestic demand and income growth. Within the Services PMI, new orders and business activity indices will be used to gauge the underlying strength of consumer spending and corporate activity, while employment-related components will help assess the sustainability of income growth. The significance of ADP employment data and Initial Jobless Claims lies less in predicting the Nonfarm Payrolls report and more in recalibrating market expectations regarding labor market conditions. These indicators help investors reassess the pace of economic moderation and adjust growth expectations accordingly.

Ultimately, market pricing will converge on the core labor market data set, including Nonfarm Payrolls, the unemployment rate, and average hourly earnings. Together, these variables determine the interaction between economic growth momentum and inflation persistence. Payroll growth influences the trajectory of economic expansion, the unemployment rate reflects labor market tightness, and wage growth directly feeds into inflation expectations. Through its impact on real interest rates and term premiums, wage growth also influences the shape of the Treasury yield curve. From an asset-pricing perspective, this data set not only affects expectations for future interest-rate policy but also reshapes equity discount-rate assumptions and credit-spread pricing, giving it broad cross-asset repricing significance.

Week’s Key Economic Data & News Recap

Treasury Yield Consolidation and the Reaffirmation of Valuation Constraints

Throughout the week, the U.S. 10-year Treasury yield traded largely within the 4.4%–4.6% range, with movements in real yields remaining the most important marginal variable for equity markets. The absence of a meaningful decline in yields kept discount-rate assumptions elevated, particularly for growth-oriented equities. Meanwhile, short-term rate pricing continued to reflect expectations that policy easing would occur later rather than sooner. As a result, markets remained in a phase of digesting a stable high-rate environment rather than adjusting to a new directional shift in interest rates.

Late-Stage Earnings Season: From Earnings Delivery to Forward-Guidance Pricing

The S&P 500 earnings season entered its final phase, with overall earnings growth remaining in the 7%–10% year-over-year range. However, sector divergence became increasingly pronounced. Consumer-related industries and selected industrial segments showed signs of stabilization following inventory normalization, while earnings volatility remained elevated in more cyclical sectors. Investor sensitivity shifted noticeably toward forward guidance, with a growing number of companies expressing caution regarding demand conditions in the second half of 2025. Consequently, the dominant market theme became a combination of solid earnings results paired with conservative outlooks.

Accelerating Capital Rotation: ETF Flow Concentration and Style Rotation

ETF fund flows remained highly selective throughout the week. Defensive sectors and high-quality assets continued to attract net inflows, while higher-volatility growth segments experienced alternating periods of outflows and renewed buying interest. The VIX remained relatively subdued within the 12–14 range, suggesting stable index-level volatility. However, individual stock volatility increased, reflecting a market environment characterized by stable indices but rising internal dispersion. Overall, investor behavior appeared more tactical in nature rather than indicative of a broad strategic asset allocation shift.

Continued Strength in AI Infrastructure Spending and CapEx Expectations

Markets continued to absorb evidence that capital expenditure plans among major cloud providers and semiconductor-related companies remain intact. In particular, there were few signs of slowing investment in data-center infrastructure. Supply-chain feedback suggested that demand remains concentrated in high-end GPUs and networking equipment, supporting elevated expectations for related industry orders. At this stage, the key driver is not the emergence of a new narrative, but rather the ongoing validation of the existing AI investment thesis.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index traded largely within the 34,250.00–34,750.00 range, posting a 5-day gain of 0.86%. The index briefly pulled back toward the 34,300 level midweek before rebounding steadily as capital flows returned to the market. By the end of the week, it had once again approached its historical highs. Overall, Canadian equities exhibited a pattern of “recovery following a pullback, with a gradual upward bias amid continued consolidation.”

Source: Yahoo Finance

U.S. Equities:

Last week, the three major U.S. equity indices maintained an upward trend amid volatile trading conditions. The S&P 500 Index gained 1.80% over the five-day period, while the NASDAQ Composite outperformed with a 2.58% advance, supported by continued strength in large-cap technology stocks. Meanwhile, the Dow Jones Industrial Average traded largely within the 50,300–51,050 range and posted a 1.49% weekly gain. Overall, improving risk sentiment, resilient corporate earnings expectations, and continued investor interest in growth-oriented sectors contributed to a market environment characterized by “steady gains following consolidation, with technology stocks leading the advance.”

Source: Yahoo Finance

U.S. Bonds:

Last week, the U.S. 10-year Treasury yield trended lower amid continued volatility, declining from approximately 4.56% at the beginning of the week to 4.453% by week’s end, representing a 2.30% decrease over the five-day period. From a technical perspective, the yield briefly moved back above the 4.50% level during the middle of the week before retreating sharply and subsequently consolidating within the 4.43%–4.46% range during the latter part of the week. Overall, easing upward pressure on long-term interest rates provided support for risk assets, while the bond market exhibited a pattern of “pullback from recent highs followed by stabilization.”

Source: Yahoo Finance

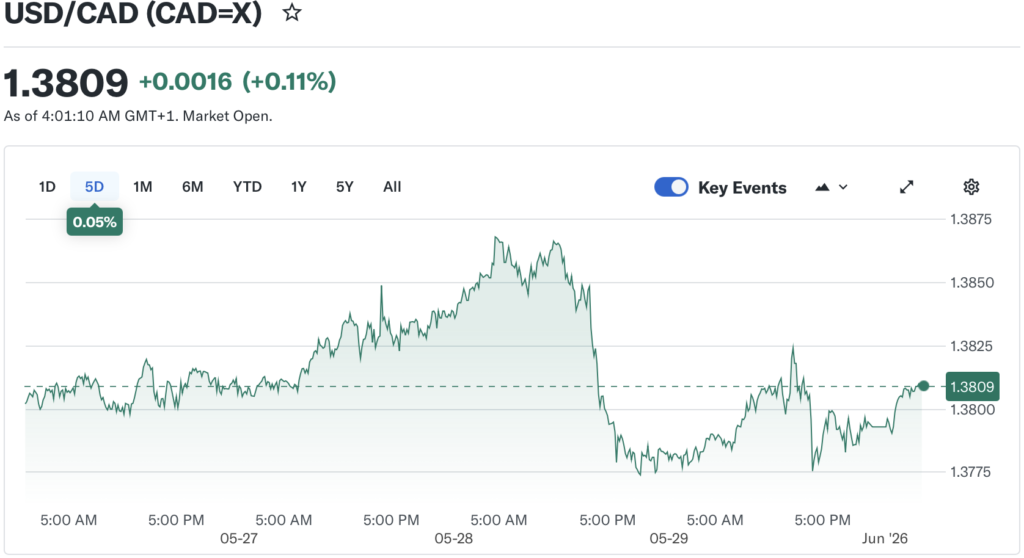

Forex Market:

Last week, the USD/CAD exchange rate traded largely within the 1.3775–1.3870 range, posting a 0.05% gain over the five-day period.

Source: Yahoo Finance

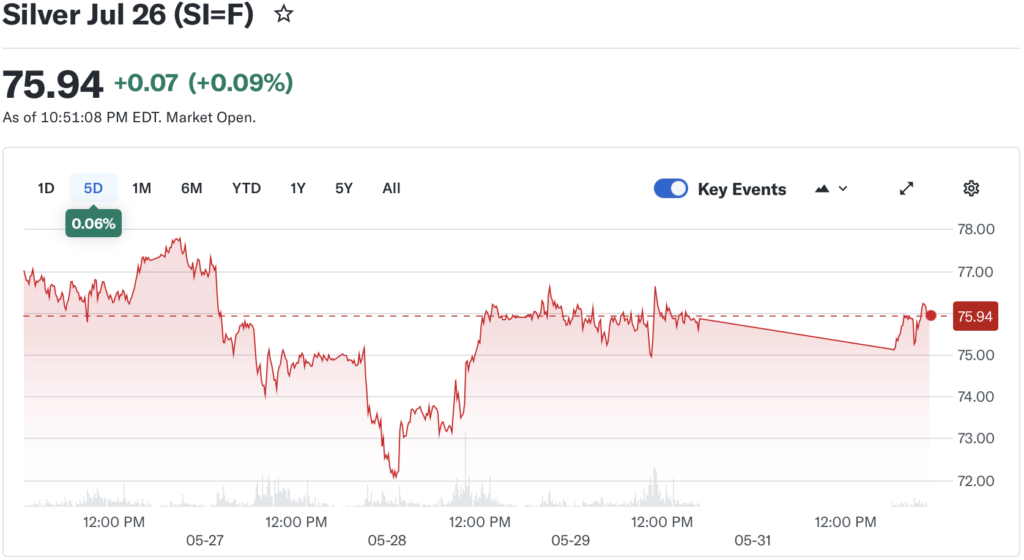

Gold & Silver Market:

Last week, the gold and silver markets remained in a high-level consolidation phase with a slightly weaker tone. Gold Futures traded largely within the $4,400–$4,610 range, closing near $4,553.20 and posting a 0.71% gain over the five-day period. Silver Futures traded within the $72.0–$77.8 range, closing near $75.94 and recording a 0.06% gain over the same period.

Source: Yahoo Finance

Oil Market:

Last week, the international oil market remained under pressure and trended lower. Brent Crude Oil Futures traded largely within the $90.00–$97.80 per barrel range, closing near $93.02 per barrel and posting a 10.16% decline over the five-day period.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of June 1st, 2026, 12:30 PM EST

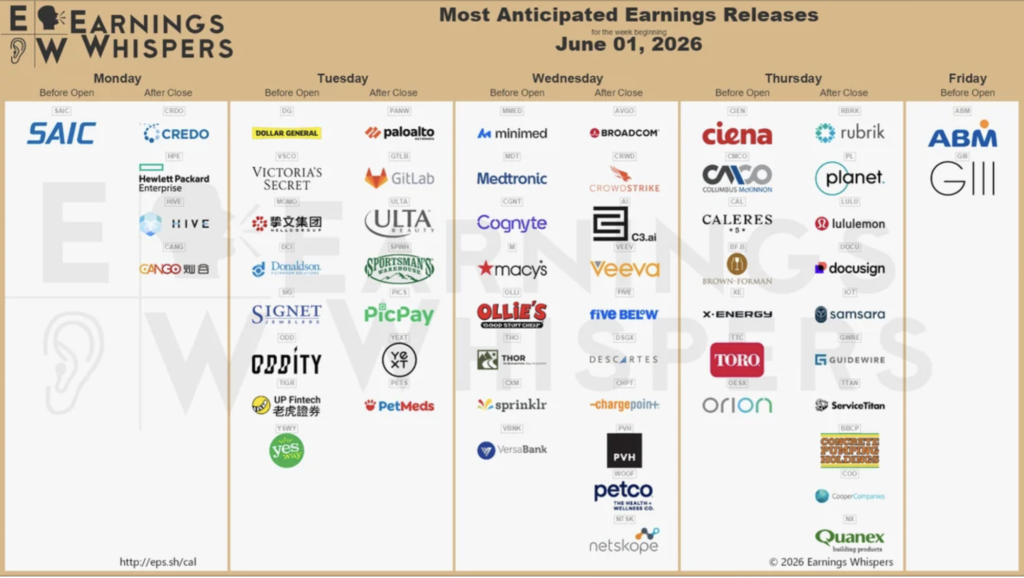

WHAT'S HAPPENING THIS WEEK

Upcoming Events (June 1 – June 5, 2026)

June 1 (Monday)

• SAIC, Credo Technology, and Hewlett Packard Enterprise (HPE) report earnings

June 2 (Tuesday)

• Dollar General, Victoria’s Secret, Donaldson, and Signet Jewelers report earnings

• Palo Alto Networks, GitLab, and Ulta Beauty release results after market close

• Markets will focus on changes in U.S. consumer spending, as well as growth trends in the cybersecurity and enterprise software sectors

June 3 (Wednesday)

• Medtronic, Macy’s, and Ollie’s Bargain Outlet report earnings

• Broadcom, CrowdStrike, Veeva, Five Below, PVH, and ChargePoint release results after market close

• CrowdStrike’s earnings will provide insight into corporate cybersecurity spending trends, while ChargePoint’s results will offer important clues regarding demand for EV charging infrastructure

June 4 (Thursday)

• Ciena, Caleres, Toro, and Orion report earnings

• Rubrik, Planet Labs, lululemon, DocuSign, Samsara, Guidewire, and ServiceTitan release results after market close

• lululemon’s earnings will serve as an important indicator of North American consumer demand and the premium retail market

June 5 (Friday)

• ABM Industries, G-III Apparel, and Quanex Building Products report earnings

Author by: Sarah San

Edited & Published by: Sarah San

June 1st , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.