Saving and investing: they’re words that people sometimes use interchangeably. But they’re definitely not the same. Saving is putting aside money to reach your goals. Investing is putting your money into something specific with the expectation that its value will grow over time, providing you with the opportunity to create more wealth.

So it’s not “Saving vs. Investing,” or “Saving = Investing.” They’re parts of the same solution. Here’s how they can work together to help you reach your goals.

Saving

For most of us, saving money means putting it into a bank account. Ideally, you don’t touch the money that’s in that account until you’ve reached the amount you need.

Part of what helps your savings grow is compounding. Assuming you’re not just hiding your money in a futon, you will be getting some kind of return on it. Savings accounts at a bank typically pay a small amount of interest on the money you deposit. And that interest keeps coming, even paying interest on the interest you’ve already earned.

But there are drawbacks to the typical savings account. First, you may be charged fees for holding the account or any transactions.

And over time, there’s another factor working against you: inflation. As you’ve probably noticed, almost every year most things get a little more expensive, and as a result your money is worth a little bit less. Inflation is typically estimated at 2% a year.

So between fees and inflation, if you’re only earning a percentage point or two in your savings account, your money isn’t growing much, and it may even shrink in value. That may not be a problem if you’re saving for a short-term goal such as a car, furniture or a big trip. But what if you’re saving for something a few years down the road, such as buying a home or retiring?

Investing

That’s where investing comes in. Rather than leaving your savings in a bank account, you can buy investments with that money.

Investing allows your wealth to grow at a much higher rate than it could in a savings account. For example, a savings account could generate an annual return between 0.05% and 2.00%. When you compare that to a typical market-tracking index account – like one that follows the S&P/TSX Composite, with its average annual return of 4.6%* – it’s clear that you could be missing out.

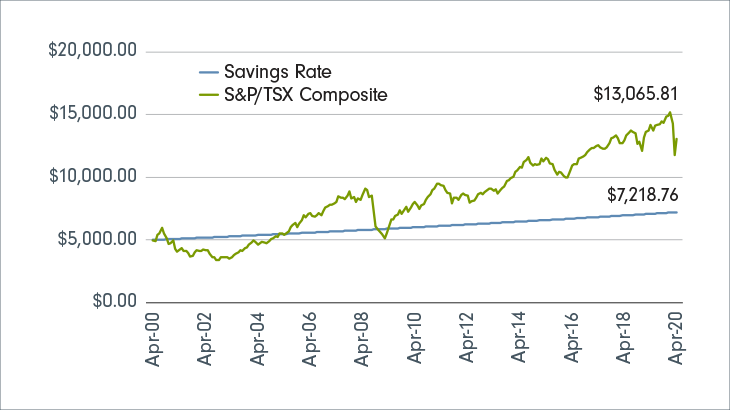

Historically, if you invest for the long term, your money will grow a lot more than if you hadn’t invested. The chart below shows what would have happened if you had invested $5,000 in global equities between April 30, 2000, and April 30, 2020. During those years, the value of your investments would have gone up and down. But as you can see, if you had stuck with it, you’d have considerably more at the end than if you had just left your money in a savings account.

* Source: Fidelity Investments ULC.