Key Focus This Week:

“Market Shift From Growth Narratives to Earnings Delivery”

The market’s core transition this week has been a shift in investor focus from forward-looking growth narratives toward the actual delivery of earnings and the quality of corporate fundamentals. This divergence has been particularly evident within the technology and AI sectors. Companies such as Alphabet and Amazon have gained market support by translating AI demand and cloud expansion into tangible revenue growth and operational results. In contrast, companies with elevated capital expenditures and unclear near-term monetization pathways are increasingly facing valuation pressure. Overall, the market is gradually transitioning from a narrative-driven environment to one that is fundamentally earnings-driven.

At the same time, companies across the energy, industrial, and consumer sectors are broadly experiencing a “revenue growth but margin pressure” dynamic, highlighting rising cost pressures as a key market variable. Even with oil prices remaining relatively elevated, the earnings performance of Exxon Mobil and Chevron continues to be affected by higher operating costs, inventory cycles, and pricing lag effects. As a result, investors are placing greater emphasis on cash flow quality, operational efficiency, and cost management capabilities. Valuation frameworks are increasingly shifting away from broad industry momentum toward the underlying quality of corporate fundamentals.

From a market structure perspective, headline index stability continues to mask significant internal divergence beneath the surface. A small group of mega-cap leaders, led by NVIDIA, continues to contribute disproportionately to overall index performance, driving higher market concentration. This structure implies that broader market performance is becoming increasingly dependent on a limited number of heavyweight companies. Consequently, any earnings disappointment from these core leaders could have an amplified impact on the overall market. In this environment, the market has clearly entered a structural stock-picking phase, where investment opportunities are increasingly driven by disciplined analysis of earnings quality, capital efficiency, and balance sheet strength, rather than broad sector allocation alone.

Week’s Key Economic Data & News Recap

Earnings Season Triggers a Broad Market Repricing

The key market driver last week was the wave of concentrated earnings releases, which created a series of rapid repricing events across equities. From Microsoft, Meta, and Alphabet on April 29, to Amazon and Apple on April 30, followed by AMD, Super Micro Computer, and Palantir on May 5, the market was forced to absorb earnings performance and capital expenditure signals from multiple layers of the AI ecosystem within a very short period of time. This high-frequency event cycle made stock performance increasingly dependent on the gap between actual results and market expectations, accelerating internal market divergence.

AI Capital Rotation Expands Beyond Chips Into Infrastructure

One of the most notable developments last week was the market’s shifting focus within the AI trade. Investor attention began moving beyond GPUs and semiconductors toward the broader AI infrastructure ecosystem. While NVIDIAremained at the center of the AI narrative, storage-related companies such as Western Digital and Seagate significantly outperformed expectations as investors increasingly recognized that the true bottleneck for AI is no longer limited to compute power alone, but also includes power supply, data storage, and data transmission capacity. In other words, the AI investment thesis is evolving from a narrow focus on “who builds the chips” toward a broader focus on “who enables AI systems to operate at scale.”

U.S. Equities Reach New Highs While Market Breadth Weakens

Although U.S. equity indices continued to reach new highs last week, internal market breadth deteriorated significantly. Recent data indicates that nearly 70% of the latest gains in the S&P 500 were driven by a small group of mega-cap technology companies, while the percentage of stocks outperforming the index has fallen to one of the lowest levels seen in nearly three decades. This divergence highlights an increasingly fragile market structure: while headline indices appear strong, a large portion of individual stocks are not participating in the rally. The market’s growing dependence on a handful of dominant technology leaders implies that any earnings disappointment from these core companies could amplify volatility across the broader market.

Across industrial and consumer sectors, companies generally reported stable revenue but faced margin pressure due to rising costs. Some transportation and travel companies lowered guidance due to higher energy expenses, while retailers and consumer firms relied on price increases and cost optimization to sustain profitability. In this environment, pricing power and cost control have become critical determinants of stock performance, with the market shifting its focus from top-line growth to earnings quality and operational efficiency.

Oil Prices Re-Emerge as a Core Trading Variable

Oil prices and geopolitical developments once again became dominant drivers of market sentiment last week. Following stalled negotiations between the United States and Iran, Brent crude briefly moved back toward the USD 100 per barrel level, reigniting concerns surrounding energy costs and a potential resurgence in inflation pressures. As a result, energy and materials sectors outperformed in the short term, while airlines, consumer-related businesses, and transportation stocks came under pressure. This shift suggests that the market has resumed actively pricing the earnings implications of a sustained higher oil-price environment, rather than treating oil movements as temporary headline-driven volatility.

Investors Begin Questioning Whether AI Spending Is Becoming Excessive

While AI remains the market’s dominant long-term theme, a growing concern emerged last week regarding whether AI-related capital spending is becoming overheated. Major technology companies including Google, Meta, Amazon, and Microsoft are collectively expected to invest close to USD 700 billion in AI-related infrastructure and development over the coming years. Investors are increasingly reassessing how long it will take for these massive investments to translate into sustainable earnings growth and free cash flow generation. Put differently, the market narrative is evolving from “AI will inevitably grow” toward a more disciplined question: “Will the scale of AI investment ultimately justify the returns?”

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

From the performance of the S&P/TSX Composite Index, the index closed last week at 34,272 (+0.57%) and showed a clear breakout above its previous trading range on the final trading day. Technically, the market is exhibiting an accelerated upward trend following a period of consolidation and gradual recovery. Compared with the repeated sideways trading seen in previous weeks, this latest advance appears more directional, suggesting that market sentiment has improved to some extent and that capital is gradually rotating back into risk assets.

Source: Yahoo Finance

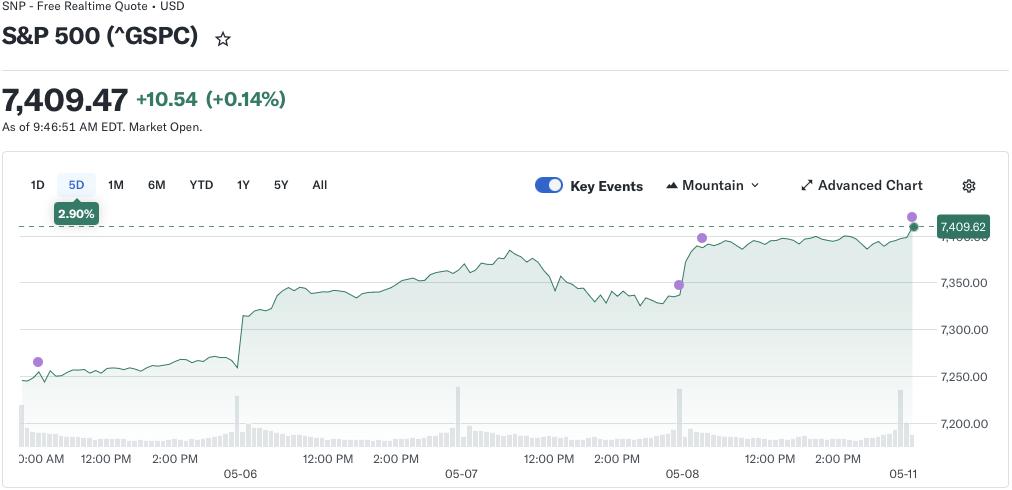

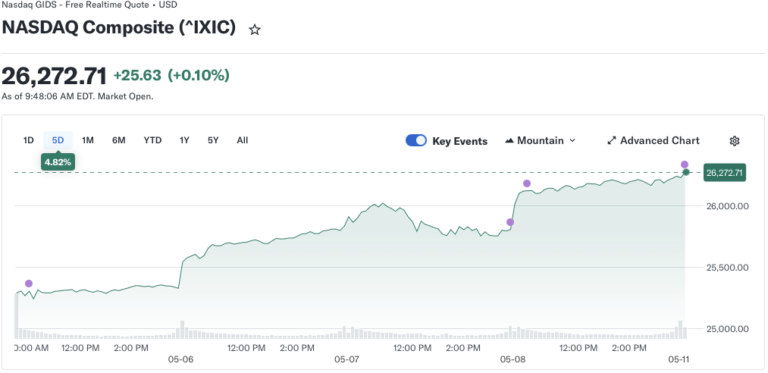

U.S. Equities:

Source: Yahoo Finance

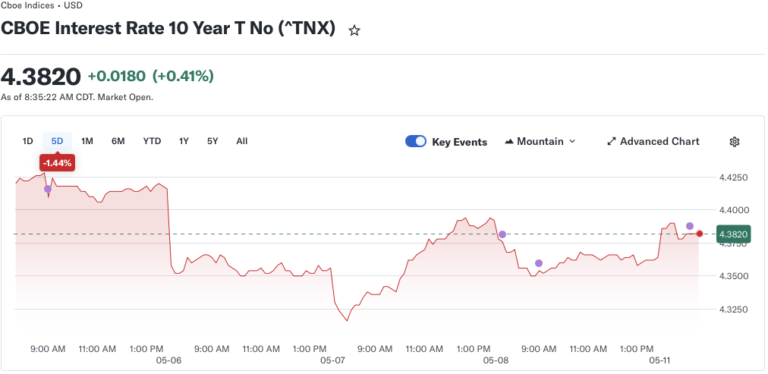

U.S. Bonds:

From the performance of the CBOE Interest Rate 10 Year T Note, the 10-year U.S. Treasury yield closed last week at 4.38% (+0.41%), showing a pattern of initial weakness followed by a gradual rebound. After briefly declining to around 4.32% during the middle of the week, yields rebounded quickly and moved back into the 4.35%–4.40% range during the second half of the week. This suggests that market expectations regarding the future interest rate path remain unstable, while the overall rate environment has not yet shown a meaningful downward shift.

Source: Yahoo Finance

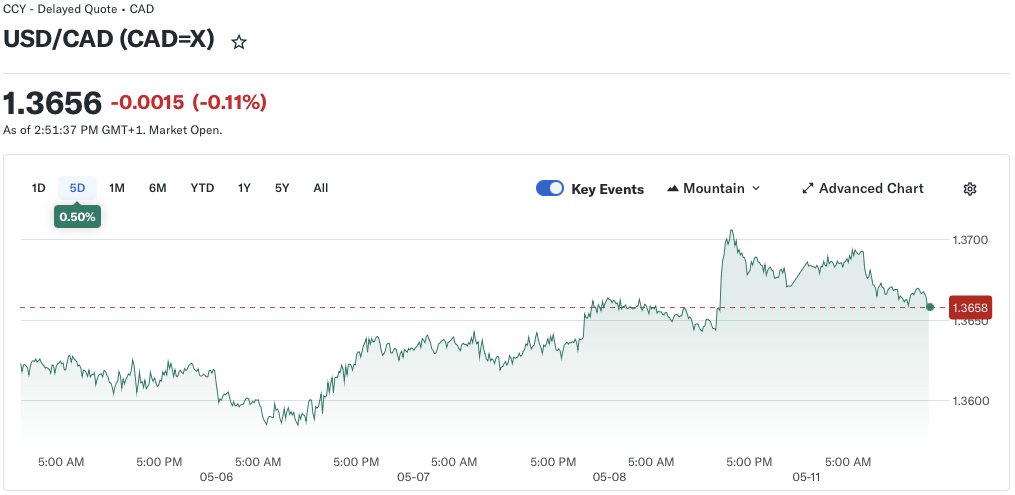

Forex Market:

The USD/CAD exchange rate is currently trading within the 1.36–1.37 range, without establishing a clear short-term directional trend. This suggests that the market remains divided on expectations surrounding interest rate differentials and commodity prices, leaving capital flows in a relatively cautious, wait-and-see mode. Overall, last week’s foreign exchange market reflected a balanced environment: the U.S. dollar remained relatively firm but lacked strong momentum, while the Canadian dollar continued to find support yet showed limited upside strength. In the near term, market direction will likely remain dependent on the evolving interest rate outlook and fluctuations in oil prices.

Source: Yahoo Finance

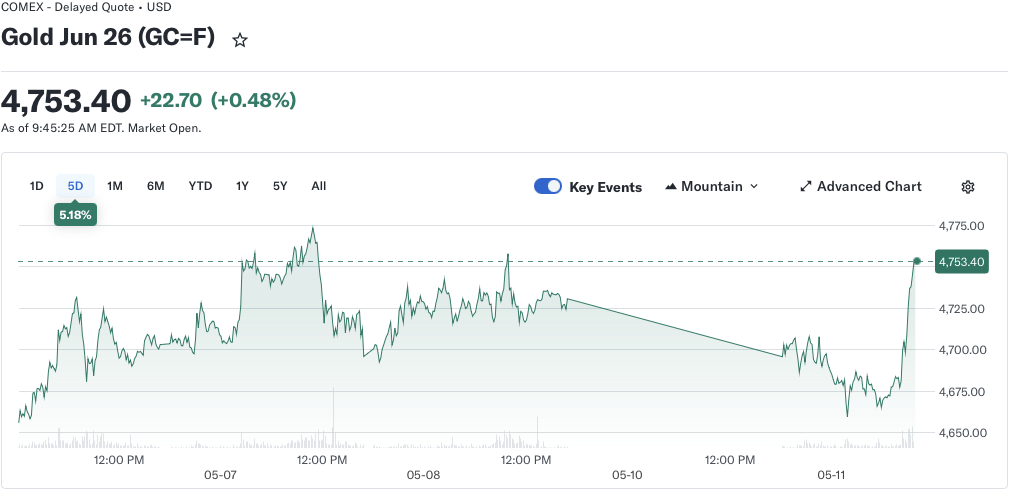

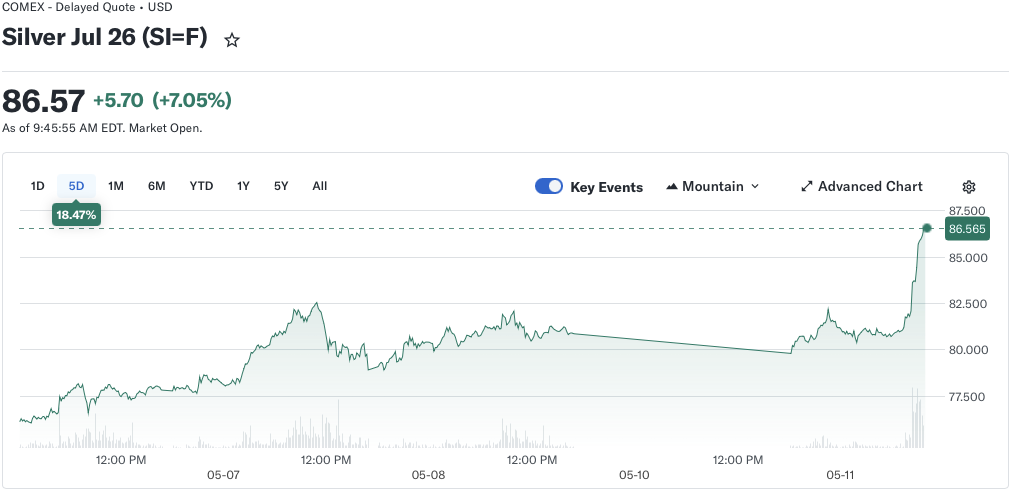

Gold & Silver Market:

From the performance of Gold Futures, gold closed last week at 4,753 (+5.18%), displaying a technical structure characterized by consolidation followed by a sharp upward breakout. Prices briefly pulled back into the 4,680–4,700 range during the middle of the week, but rebounded strongly in the latter half of the week and broke above the upper boundary of the previous consolidation range, indicating renewed capital inflows into safe-haven assets. This type of price action typically reflects a reassessment of market uncertainty and the interest rate outlook, leading to renewed allocation demand for gold.

At the same time, Silver Futures significantly outperformed, closing at 86.57 (+18.47%), far exceeding gold’s gains and demonstrating a classic high-beta catch-up rally structure. Silver traded sideways during the first half of the week but accelerated sharply higher toward the end of the week, suggesting that market risk appetite improved while capital began rotating from defensive assets toward more volatile precious metals exposure.

Source: Yahoo Finance

Oil Market:

From the performance of Brent Crude Oil Futures, oil prices closed last week at 102.97 (-10.02%), exhibiting a market structure characterized by a sharp selloff followed by a period of volatile stabilization and partial recovery. At the beginning of the week, prices fell rapidly toward the USD 95 range before gradually rebounding. However, oil prices consistently failed to reclaim previous highs above USD 105, suggesting that although some buying interest emerged after the emotionally driven selloff, overall upside momentum remained clearly limited.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of May 11, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (May 4 – May 8, 2026)

May 11 (Monday) | Validation of Resources and Small-Cap Growth Sectors

- Barrick Gold, Mosaic, and Rigetti Computing are scheduled to report earnings.

- Investors will focus on how commodity prices — particularly gold and fertilizer prices — are translating into corporate earnings performance, while also evaluating cash flow pressure and commercialization progress among high-growth technology companies such as those involved in quantum computing.

May 12 (Tuesday) | Validation of China and Emerging Technology Supply Chains

- JD.com, Sea Limited, and Kopin Corporation are scheduled to release earnings.

- Key areas of focus include the recovery trajectory of Chinese consumption and e-commerce activity, whether demand for emerging technologies such as AR, hardware, and digital platforms is improving, and how global demand conditions are impacting cross-border businesses.

May 13 (Wednesday) | Validation of Technology Infrastructure and Enterprise IT Spending

- Cisco Systems, Wix.com, and Dynatrace are expected to report earnings.

- Markets will closely monitor whether enterprise IT spending is showing signs of recovery, whether AI-related infrastructure segments such as networking and cloud monitoring continue to benefit from AI adoption trends, and how enterprise customer budget allocations are evolving.

May 14 (Thursday) | Validation of Fintech and Platform Monetization Capabilities

- Nu Holdings, Klarna, and Applied Materials are scheduled to announce earnings.

- Investors will focus on the profitability and user growth quality of fintech platforms, as well as whether demand for semiconductor equipment — particularly within the capital expenditure cycle — remains resilient.

May 15 (Friday) | Final Validation of Consumer and Traditional Industry Trends

- Alaska Air Group, YETI Holdings, and RBC Bearings are scheduled to report earnings.

- Key themes include the resilience of consumer demand in areas such as travel and outdoor spending, as well as changes in industrial orders and inventory cycles, which may provide broader signals regarding the strength of real economic activity.

Author by: Sarah San

Edited & Published by: Sarah San

May 11th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.