Key Focus This Week:

“Federal Reserve Decision, Retail Sales, and Inflation Pressures Take Center Stage”

This week, market attention will focus on the Federal Reserve’s June policy meeting, U.S. retail sales data, and whether inflationary pressures remain elevated. Last week’s CPI and PPI reports indicated that inflation remains well above the Federal Reserve’s 2% target, with energy prices continuing to be a key driver of price increases. Although U.S. equities rebounded on Friday amid optimism surrounding SpaceX’s market debut and easing geopolitical tensions in the Middle East, investors remain focused on whether persistent inflation will keep the Federal Reserve on a hawkish policy path.

On the monetary policy front, the Federal Open Market Committee (FOMC) will meet on June 16–17 and release its interest rate decision along with updated economic projections. Following May CPI rising 4.2% year-over-year and PPI increasing 6.5% year-over-year, markets widely expect the Fed to leave rates unchanged. However, investors will closely scrutinize the policy statement, updated dot plot, and Chair Powell’s press conference for signals regarding inflation, labor market conditions, and the future path of interest rates. Any indication that the Fed intends to maintain restrictive policy for longer could reinforce expectations of a prolonged higher-rate environment.

From an economic data perspective, May Retail Sales will be released on June 17 and will provide fresh insight into the health of consumer spending. While the U.S. labor market has remained resilient, rising inflation and higher energy costs may be weighing on household purchasing power. A stronger-than-expected retail sales report would support the view that economic activity remains robust, while a weaker reading could increase concerns about slowing consumer demand and moderating economic growth.

In equity markets, investors will be watching whether last week’s rebound in technology stocks can be sustained. SpaceX’s strong Nasdaq debut improved market sentiment and boosted risk appetite, while reports of progress in U.S.–Iran negotiations helped alleviate concerns surrounding global energy supply disruptions. Nevertheless, technology stocks have already experienced a period of consolidation, and investors remain focused on valuation pressures facing AI-related and high-growth sectors in a higher-rate environment. Over the coming days, Treasury yields, the Fed’s policy messaging, and capital flows into the technology sector are likely to determine the market’s near-term direction.

Week’s Key Economic Data & News Recap

U.S. May CPI Rises to 4.2% YoY as Energy Prices Drive Inflation Higher

According to data released by the U.S. Bureau of Labor Statistics last Wednesday, the Consumer Price Index (CPI) increased 0.5% month-over-month in May, compared with a 0.6% increase in April. On an annual basis, CPI rose 4.2%, up from 3.8% in April. Energy prices were the primary contributor to the increase in headline inflation, rising 3.9% month-over-month. Gasoline prices climbed 7.0% during the month and were up 40.5% over the past year, while overall energy prices increased 23.5% year-over-year.

Core inflation, which excludes food and energy, rose 0.2% month-over-month, down from 0.4% in April. On a year-over-year basis, Core CPI increased 2.9%, slightly above April’s 2.8% reading. These figures suggest that while energy prices significantly boosted headline inflation, underlying inflationary pressures remained relatively contained. As a result, market participants remain divided in their interpretation of the data. On one hand, the rebound in headline inflation could encourage the Federal Reserve to remain cautious; on the other, the absence of significant acceleration in core inflation has eased some concerns about broad-based inflationary pressures.

U.S. May PPI Climbs 6.5% YoY as Producer Price Pressures Intensify

The Producer Price Index (PPI) report released last week showed that final demand PPI increased 1.1% month-over-month and 6.5% year-over-year in May. Final demand goods prices rose 2.8%, while services prices increased 0.3%. Energy-related components recorded particularly strong gains, with energy prices rising 10.7%, gasoline prices increasing 23.4%, and diesel prices advancing 15.7% during the month.

The PPI data indicates that pricing pressures at the producer level remain elevated, particularly in energy and raw materials. Investors are concerned that continued increases in production costs could eventually be passed through to consumers, potentially slowing the pace of disinflation. This has reinforced expectations that the Federal Reserve will maintain a cautious policy stance in the near term.

U.S. Equities Rebound Friday as Market Sentiment Improves

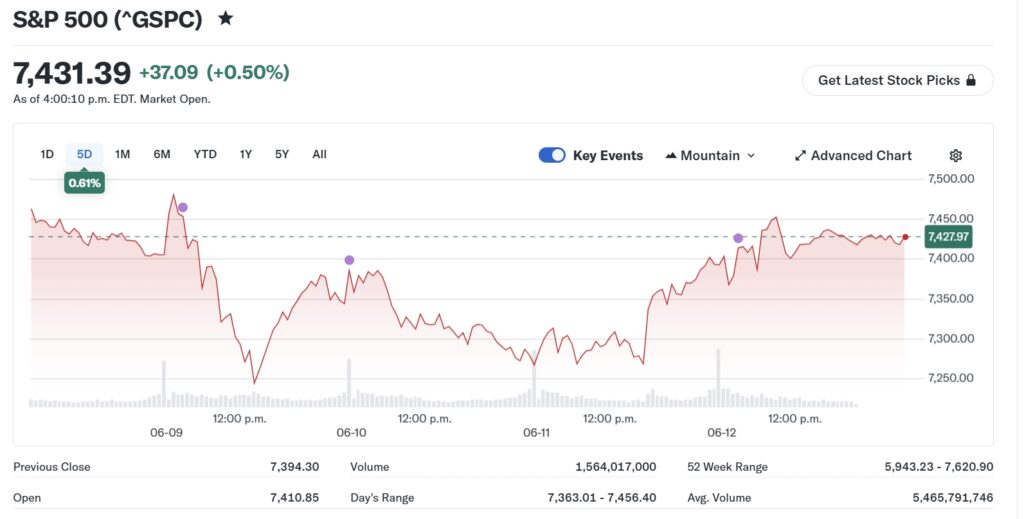

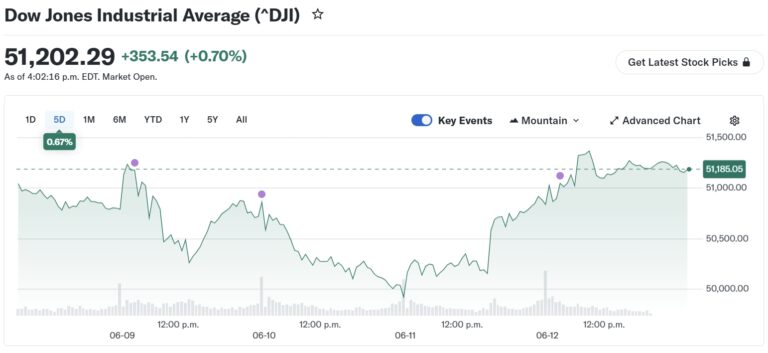

U.S. equity markets closed higher on Friday, supported by strong investor enthusiasm surrounding SpaceX’s public market debut and easing geopolitical tensions in the Middle East. The Dow Jones Industrial Average gained 0.70% to close at 51,202.26, the S&P 500 rose 0.50% to 7,431.46, and the Nasdaq Composite advanced 0.31% to 25,888.84. While Friday’s rally helped improve sentiment, overall weekly performance remained mixed, particularly within the technology sector, where volatility persisted.

The market’s advance was driven by two primary factors. First, reports suggesting that the United States and Iran were nearing an agreement reduced concerns about potential disruptions to shipping through the Strait of Hormuz and eased fears of further energy-driven inflation. Second, SpaceX’s highly successful market debut generated significant investor interest and supported broader sentiment across technology and growth-oriented sectors.

SpaceX IPO Becomes the Week’s Most Significant Capital Markets Event

SpaceX began trading on Nasdaq on Friday and delivered a strong first-day performance, making it one of the most closely watched capital markets events of the year. The company’s successful listing highlighted continued investor appetite for innovative technology and high-growth businesses while increasing attention on the commercial space industry.

At the same time, investor focus has increasingly shifted from pure revenue growth toward profitability, capital efficiency, and valuation discipline. In the current higher-interest-rate environment, market participants are placing greater emphasis on earnings visibility, returns on capital investment, and the long-term sustainability of business models. As a result, although growth-oriented technology companies continue to benefit from improving risk sentiment, valuation pressures remain a key consideration.

Oil Prices Retreat, Easing Some Inflation Concerns but Remaining a Key Variable

Last week, optimism surrounding potential progress in U.S.–Iran negotiations helped reduce concerns about global energy supply disruptions and contributed to a pullback in crude oil prices. Lower energy prices improved overall market sentiment and helped alleviate fears of further acceleration in inflation.

However, both the CPI and PPI reports highlighted that energy costs remain a major contributor to inflationary pressures. As a result, developments in the energy market will continue to play a significant role in shaping inflation expectations and influencing future Federal Reserve policy decisions.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index remained in an upward trading range between 34,436.70 and 35,078.00, posting a gain of approximately 1.5% over the week. Strength across the financial, energy, and materials sectors helped drive a broad-based recovery from mid-week lows, pushing the index back toward all-time highs. The overall market structure reflected a constructive rebound following a brief consolidation phase, supported by resilient commodity prices and renewed risk appetite among investors.

Source: Yahoo Finance

U.S. Equities:

Last week, the three major U.S. equity indices moved higher in a broadly upward trading pattern. The S&P 500 Index traded within a range of approximately 7,250 to 7,460, gaining 0.61% over the five-day period. The Nasdaq Composite advanced 0.71%, trading between 25,000 and 26,000, while the Dow Jones Industrial Average rose 0.67%, fluctuating within the 49,900 to 51,300 range. After experiencing a brief mid-week pullback, all three indices quickly recovered and moved back toward record-high levels.

Source: Yahoo Finance

U.S. Bonds:

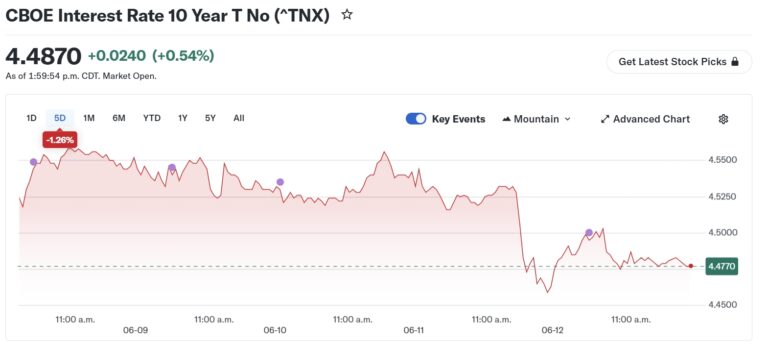

Last week, the CBOE 10-Year Treasury Note Yield (^TNX) traded within a range of approximately 4.46% to 4.56%, declining about 1.26% over the five-day period. The yield briefly fell to around 4.46% during the week before closing near 4.48%. Overall, U.S. long-term interest rates reversed their previous upward trend as investors reassessed the outlook for monetary policy and adjusted expectations regarding the future path of Federal Reserve interest rates.

Source: Yahoo Finance

Forex Market:

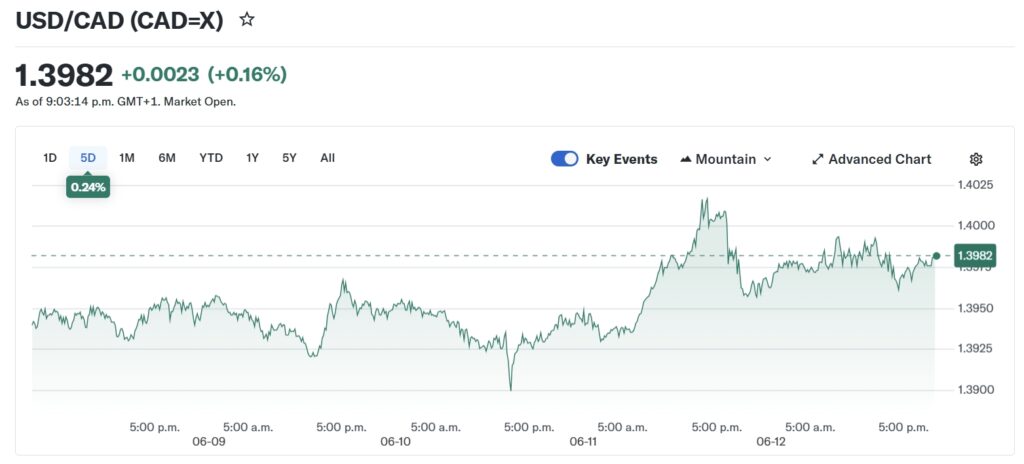

Last week, USD/CAD traded within a range of approximately 1.3926 to 1.3995, posting a gain of about 0.24% over the five-day period. The currency pair briefly climbed toward the 1.4010 level during the week before closing near 1.3972. Overall, the U.S. dollar continued its recent rebound against the Canadian dollar, supported by resilient U.S. economic data and persistent interest rate differentials between the two countries.

Source: Yahoo Finance

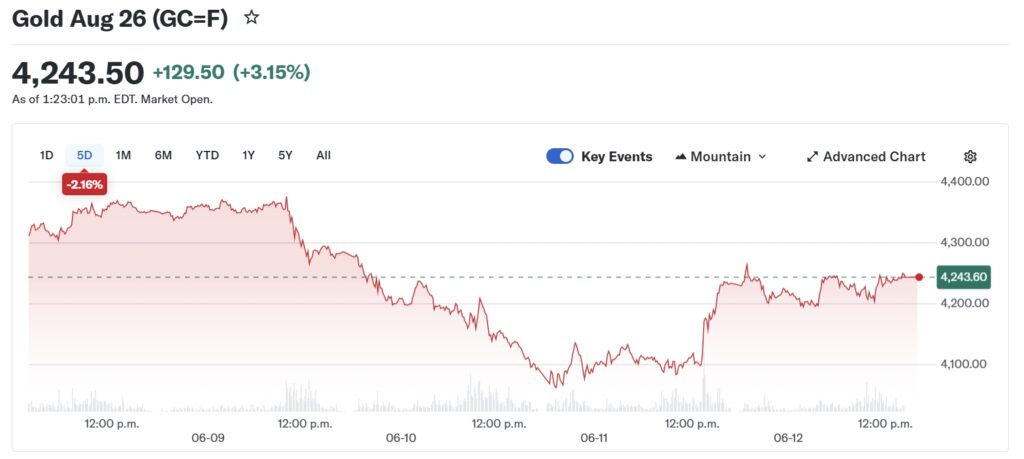

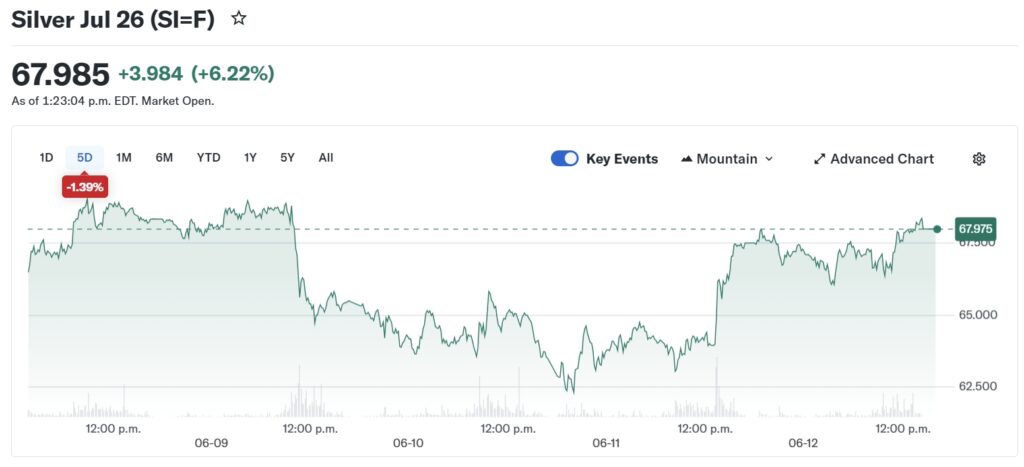

Gold & Silver Market:

Last week, Gold Futures (GC=F) traded within a range of approximately 4,060 to 4,370, declining about 2.16% over the five-day period. Gold briefly fell to around 4,070 during the week before rebounding sharply to close near 4,244. Meanwhile, Silver Futures (SI=F) fluctuated between 62.5 and 68.0, posting a weekly decline of approximately 1.39% and finishing the week near 67.98. Overall, precious metals regained buying support following a mid-week pullback, with both gold and silver continuing to trade near historically elevated levels.

Source: Yahoo Finance

Oil Market:

Last week, Brent Crude Oil Futures (BZ=F) traded within a range of approximately USD 85.5 to USD 96.5 per barrel, declining about 6.21% over the five-day period. Oil prices briefly fell toward the USD 85 level during the week before closing near USD 87.3 per barrel. Overall, global crude oil prices reversed their previous rebound and experienced a notable correction, as concerns over slowing demand growth and a decline in market risk appetite weighed on sentiment across the energy sector.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of June 15th, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (June 15 – June 19, 2026)

June 15 (Monday)

• Earnings releases from Domo, Canopy Growth, High Tide, PowerFleet, RF Industries, Quantum, and others.

June 16 (Tuesday)

• Earnings releases from Vince Holding, John Wiley & Sons, La-Z-Boy, and others.

June 17 (Wednesday)

• Earnings releases from Progressive, Jabil, CarMax, and others.

• The U.S. will release Retail Sales, Business Inventories, and Pending Home Sales data.

• The Federal Open Market Committee (FOMC) interest rate decision will be announced in the afternoon, followed by the Fed Chair’s press conference.

June 18 (Thursday)

• Earnings releases from Kroger, Accenture, and others.

June 19 (Friday)

• U.S. markets will be closed in observance of the Juneteenth National Independence Day holiday.

Author by: Sarah San

Edited & Published by: Sarah San

June 15th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.