Key Focus This Week:

“CPI Data, the Federal Reserve Policy Path, and the AI Sector Correction Take Center Stage”

Market attention this week will be focused on the U.S. May Consumer Price Index (CPI), the future path of Federal Reserve policy, and whether the AI sector can regain stability following recent weakness. Last week’s stronger-than-expected Nonfarm Payrolls report prompted investors to reassess the timing of potential Fed rate cuts. At the same time, rising U.S. Treasury yields, a stronger U.S. dollar, and less optimistic-than-expected guidance from several AI and semiconductor companies contributed to a pullback in technology stocks.

On the economic front, the U.S. May CPI report will be released this week. Investors will closely monitor the data for signs that inflation continues to move toward the Federal Reserve’s 2% target. A higher-than-expected CPI reading could reinforce concerns that interest rates may remain elevated for longer, potentially keeping Treasury yields at current high levels. Conversely, evidence of easing inflation could help alleviate concerns that future rate cuts may be delayed further.

With respect to Federal Reserve policy, investors will continue to monitor comments from Fed officials regarding labor market conditions, inflation, and the future policy outlook. Last week’s strong employment data highlighted the resilience of the U.S. economy and led markets to scale back expectations for the number of rate cuts this year. The focus of market debate has gradually shifted from “when rate cuts will begin” to “how long interest rates will need to remain elevated.”

In addition, investors will be closely following developments surrounding SpaceX’s anticipated Nasdaq listing, currently expected on June 12. According to publicly available information, SpaceX plans to raise approximately $75 billion at an offering price of $135 per share, implying a valuation of roughly $1.75 trillion and potentially making it one of the largest IPOs in history. Market participants generally view the listing as one of the most significant capital market events of the year and an important benchmark for assessing valuations across artificial intelligence, aerospace technology, and high-growth companies. A strong post-listing performance could further support sentiment toward growth-oriented technology sectors, while a weaker reception may prompt investors to reassess valuation levels across high-growth equities.

Week’s Key Economic Data & News Recap

U.S. May Nonfarm Payrolls Significantly Exceed Expectations, Highlighting Labor Market Resilience

Data released by the U.S. Bureau of Labor Statistics (BLS) last Friday showed that Nonfarm Payrolls increased by 172,000 in May, substantially exceeding market expectations. In addition, payroll figures for March and April were revised upward by a combined 93,000 jobs. The unemployment rate remained at 4.3%, while average hourly earnings increased 0.3% month-over-month and 3.4% year-over-year.

Overall, the U.S. labor market continues to demonstrate considerable resilience. Following the release of the stronger-than-expected employment data, markets further pushed back expectations for future Federal Reserve rate cuts. Several institutions lowered their forecasts for the number of cuts expected this year, contributing to higher Treasury yields and a stronger U.S. dollar. Investors increasingly began to reassess the possibility that elevated interest rates may remain in place for an extended period.

Treasury Yields Rise as Markets Reprice the Federal Reserve’s Policy Outlook

Following the employment report, U.S. Treasury yields moved notably higher. As of June 5, the 10-year U.S. Treasury yield rose to 4.54%, representing an increase of approximately 1.9% for the week.

Markets interpreted continued labor market strength as evidence that the Federal Reserve has little incentive to lower interest rates in the near term. Rising yields supported the U.S. dollar while creating headwinds for higher-valuation growth stocks. Investors increasingly returned to a “Higher for Longer” framework, with Treasury yields once again becoming a key driver of global asset pricing.

U.S. Equities Pull Back as Technology and AI Stocks Come Under Pressure

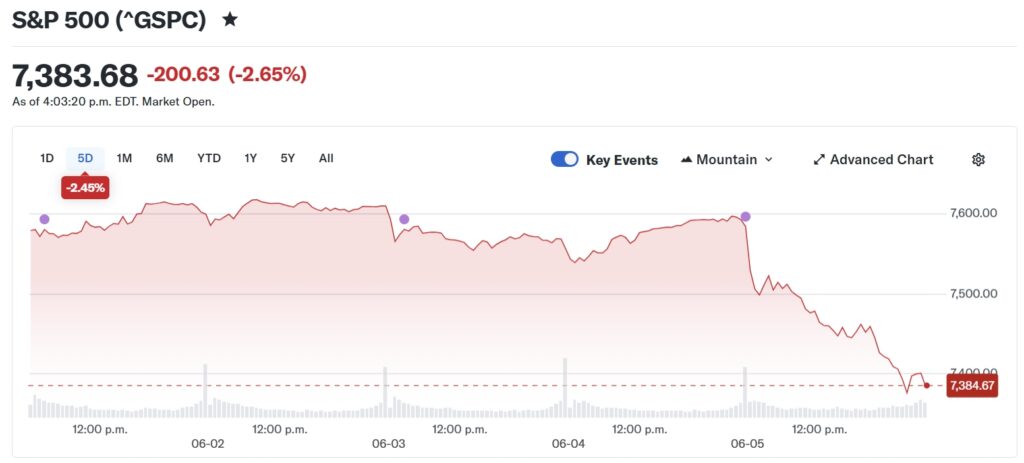

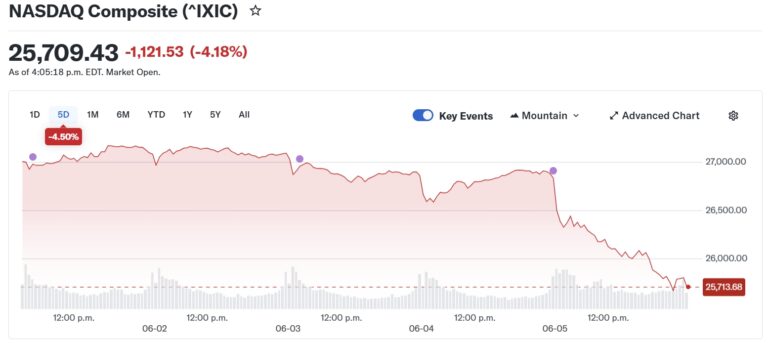

Driven by stronger employment data and shifting interest-rate expectations, major U.S. equity indices moved lower last week. As of June 6, the S&P 500 closed at 7,383.68, declining 2.45% for the week. The Nasdaq Composite fell 4.50% to 25,709.43, while the Dow Jones Industrial Average declined 0.23% to 50,866.78.

The Nasdaq’s significantly larger decline relative to the S&P 500 suggests a reduction in investor risk appetite toward high-valuation growth and technology stocks. Following its earnings release, Broadcom reported continued strong growth in AI-related semiconductor revenue; however, total revenue came in slightly below market expectations, and management did not raise its AI revenue outlook for the coming fiscal year. As a result, investors reassessed assumptions surrounding the AI capital expenditure cycle and valuation levels. The stock experienced heightened volatility following the announcement and weighed on broader semiconductor sector performance.

While investors have not abandoned the long-term AI growth narrative, market participants are increasingly focused on whether AI-related capital spending remains sustainable, whether earnings growth can justify current valuation levels, and whether future investments in data centers and cloud infrastructure can generate attractive returns. Market leadership is gradually shifting from AI growth expectations toward AI earnings realization.

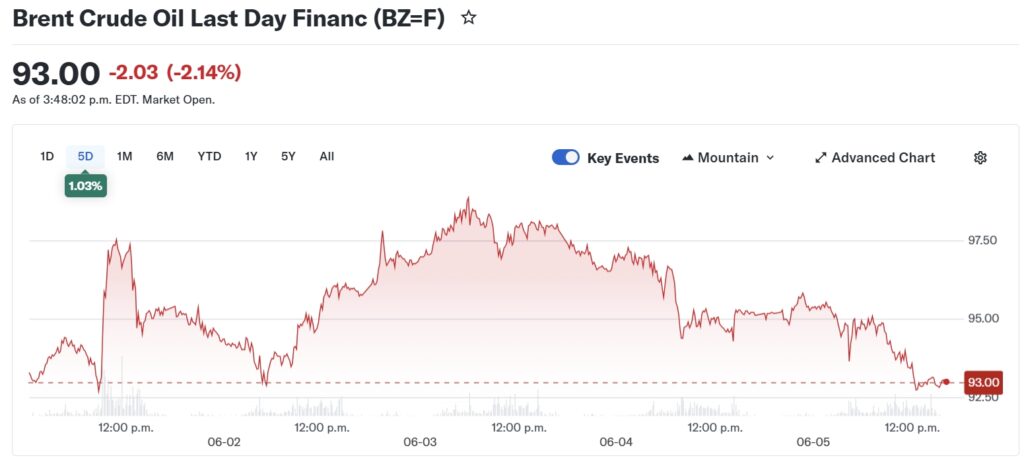

Crude Oil Remains Elevated as Inflation Risks Stay in Focus

In energy markets, Brent crude oil remained near $93 per barrel, posting a gain of approximately 1% for the week. Investors continued to monitor developments in the Middle East and the outlook for global energy supply.

Market participants remain concerned that any escalation in geopolitical tensions could push oil prices higher and reignite concerns about inflation. Given that inflation control remains the Federal Reserve’s primary objective, energy prices are expected to remain an important driver of market sentiment and inflation expectations in the months ahead.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index traded within a range of 34,379.70 to 35,291.10, posting a 1.02% decline over the five-day period. Overall, amid increasing profit-taking activity and a temporary moderation in risk appetite, Canadian equities exhibited a pattern of “retreating after reaching new highs, followed by a period of consolidation at elevated levels.”

Source: Yahoo Finance

U.S. Equities:

Last week, the three major U.S. equity indices experienced a pullback after reaching intra-week highs. The S&P 500 Index traded within a range of 7,368.63 to 7,620.90, declining 2.45% over the five-day period. The NASDAQ Composite traded between 25,648.47 and 27,190.21, posting a 4.50% loss, while the Dow Jones Industrial Average fluctuated within the 50,687.70 to 51,660.40 range and recorded a modest 0.23% decline. From a technical perspective, all three indices reached interim highs during the week before undergoing a notable correction, with technology stocks facing the most significant selling pressure. As a result, the NASDAQ substantially underperformed the broader market.

Source: Yahoo Finance

U.S. Bonds:

Last week, the U.S. 10-year Treasury yield moved higher amid continued volatility, rising from approximately 4.45% at the beginning of the week to 4.536% by week’s end, representing a 1.86% increase over the five-day period.

Source: Yahoo Finance

Forex Market:

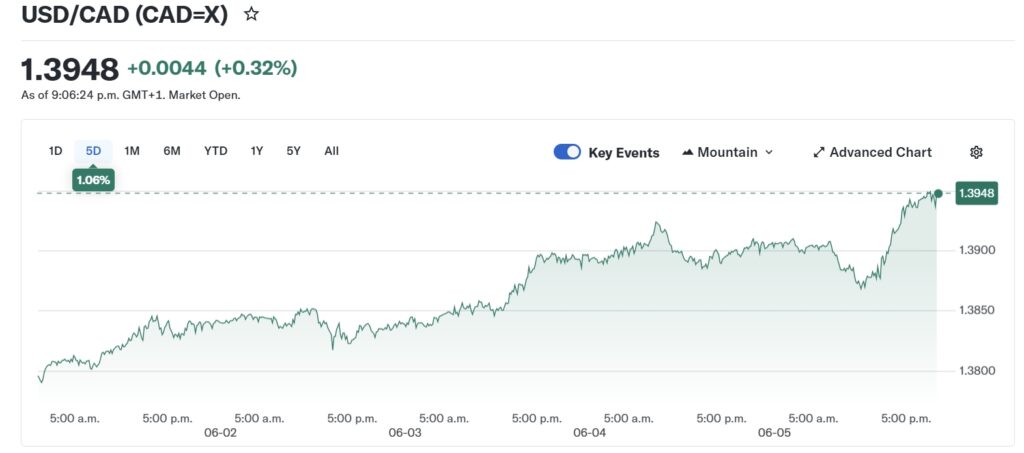

Last week, the USD/CAD exchange rate maintained an upward trend amid range-bound trading, fluctuating within the 1.3790–1.3950 range and posting a 1.06% gain over the five-day period.

Source: Yahoo Finance

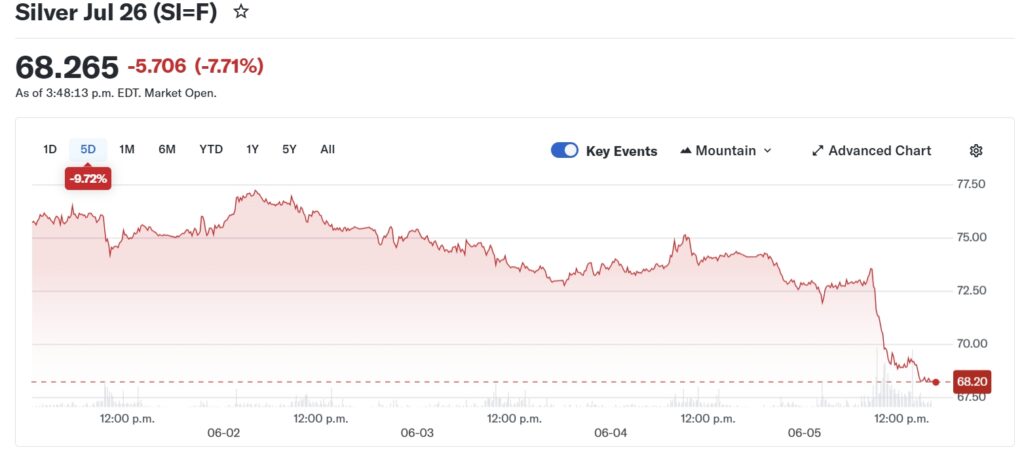

Gold & Silver Market:

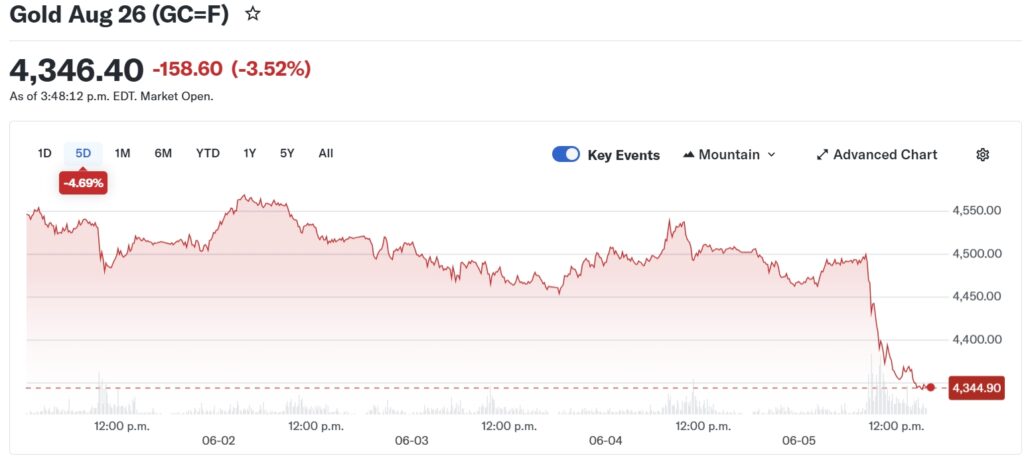

Last week, the gold and silver markets experienced a notable pullback. Gold Futures traded within a range of $4,340 to $4,560, closing near $4,346.40 and posting a 4.69% decline over the five-day period. Silver Futures traded between $68.00 and $77.50, closing near $68.27 and recording a 9.72% loss over the same period.

Source: Yahoo Finance

Oil Market:

Last week, the international oil market experienced a pullback after reaching intra-week highs. Brent Crude Oil Futures traded within a range of $92.50 to $98.50 per barrel, closing near $93.00 per barrel and posting a 1.03% gain over the five-day period. From a price-action perspective, crude oil briefly climbed to a weekly high near $98 per barrel before reversing lower. Prices continued to retreat throughout the second half of the week, breaking below the $95 level and ultimately settling near $93 per barrel by week’s end.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of June 8th, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (June 8 – June 12, 2026)

June 8 (Monday)

• FuelCell Energy, Campbell’s, Duluth Holdings, Mister Car Wash, and Graham Corporation report earnings

June 9 (Tuesday)

• Academy Sports, Casey’s General Stores, United Natural Foods (UNFI), J.M. Smucker, and Titan Machinery report earnings

• Bark, Skillsoft, Lands’ End, and Lakeland Industries release results after market close

June 10 (Wednesday)

• Chewy, J.Jill, Designer Brands (DBI), and Navient report earnings

• Oracle, Stitch Fix, Aterian, Navan, and Oxford Industries release results after market close

• Chewy’s earnings will provide insight into consumer demand within the pet care sector, while Stitch Fix’s results may offer important signals regarding discretionary consumer spending trends in the United States

June 11 (Thursday)

• Lovesac, Hooker Furnishings, Aurora Cannabis, and McGrath RentCorp report earnings

• Adobe, RH, and Lennar release results after market close

June 12 (Friday)

• Earnings season enters a relatively quieter phase, with investors continuing to assess results and forward guidance from key companies including Oracle, Adobe, and Lennar

Author by: Sarah San

Edited & Published by: Sarah San

June 8th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.