Key Focus This Week: “Markets Watch Geopolitical Developments and February Jobs Report”

As markets enter the week of March 2, investor attention is focused on two primary drivers: escalating geopolitical tensions in the Middle East and a heavy slate of U.S. economic data, led by Friday’s February employment report. The recent U.S. and Israeli military strikes on Iranian targets, followed by reported retaliatory actions, have introduced a new layer of geopolitical risk. Early market reactions have included higher oil prices and increased demand for traditional safe-haven assets, underscoring elevated uncertainty.

Beyond geopolitics, the February U.S. nonfarm payrolls report will be the most consequential scheduled release of the week. Economists expect job growth to moderate compared with January’s strong print, while wage data and the unemployment rate will be closely monitored for signals on labor market resilience. Given the Federal Reserve’s data-dependent stance, labor market conditions remain central to rate expectations and broader risk sentiment.

Additional economic indicators will provide context ahead of the jobs report. ISM manufacturing and services surveys will offer timely insight into business activity and pricing pressures, while the ADP private payrolls report may shape expectations mid-week. Retail sales data will further inform investors about consumer spending trends, a key driver of U.S. economic growth.

Corporate earnings will also continue, with select technology and consumer names reporting results. In particular, Broadcom’s earnings may serve as an additional gauge of AI-related investment demand following Nvidia’s mixed market reaction last week.

Last Week’s Key Economic Data & News Recap

Nvidia Earnings Beat Expectations, But Shares Decline

Nvidia reported fiscal fourth-quarter 2026 results that exceeded analyst expectations, highlighting continued strength in AI-driven demand. The company posted adjusted earnings per share of $1.62 versus expectations of $1.53, while revenue reached $68.1 billion, surpassing forecasts of approximately $66 billion. Data center revenue accounted for the vast majority of sales, underscoring sustained enterprise AI infrastructure investment.

Despite the strong results and forward guidance pointing to continued growth, Nvidia shares fell approximately 5% in the session following earnings, reflecting elevated investor expectations and valuation sensitivity rather than operational weakness.

Given Nvidia’s substantial weighting in major indices, the post-earnings decline weighed on the broader technology sector and contributed to weakness in the Nasdaq Composite during the latter half of the week.

U.S.–Iran Escalation Increases Geopolitical Risk Premium

Over the weekend of February 28–March 1, the United States and Israel launched coordinated military strikes on Iranian targets, marking a significant escalation in Middle East tensions. Iranian authorities subsequently reported retaliatory actions, increasing uncertainty surrounding regional stability.

Although the developments occurred after Friday’s market close, early trading at the start of the new week reflected an immediate reaction across global asset classes. U.S. equity futures traded lower, oil prices moved higher amid concerns over potential supply disruptions, and gold prices strengthened as investors sought traditional safe-haven assets. Treasury yields also declined in early trading, consistent with defensive positioning.

The escalation introduces an additional geopolitical risk factor into markets already sensitive to inflation data and technology sector volatility. While the full economic implications remain uncertain, the initial market response indicates a measurable rise in risk premiums across energy and safe-haven assets heading into the week of March 2.

Producer Price Index Surprise Reignites Inflation Concerns

U.S. wholesale inflation came in stronger than expected last week, shifting market sentiment late in the week. January’s Producer Price Index (PPI) rose 0.5% month-over-month, above the consensus estimate of approximately 0.3%, while core PPI increased 0.8%, significantly exceeding expectations.

The upside surprise suggested that upstream price pressures remain persistent, raising concerns that the Federal Reserve may not be able to ease monetary policy as quickly as markets had anticipated earlier this year. Following the release, equity markets declined and volatility increased as investors reassessed rate-cut expectations.

The inflation data reinforced the sensitivity of risk assets to incoming price data, particularly given elevated equity valuations and heavy positioning in growth-oriented sectors.

Equity Markets Turn Defensive as Inflation and Valuation Sensitivity Resurface

Equity markets entered the week with mixed momentum but shifted into a more defensive posture following the inflation surprise and technology sector weakness. The market’s midweek stabilization proved short-lived as renewed concerns about inflation persistence and valuation sensitivity pressured growth-oriented stocks.

Technology shares bore the brunt of the pullback, particularly AI-linked mega-cap names. With investor positioning elevated and earnings expectations high, the market reaction to strong corporate results underscored a growing sensitivity to valuation levels rather than fundamental growth alone.

The week’s price action reflected a broader recalibration in risk appetite. As inflation data complicated the outlook for monetary easing, investors appeared less willing to extend risk exposure, particularly in rate-sensitive sectors. The shift reinforced the dominance of macro drivers—especially inflation—in shaping short-term equity performance.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

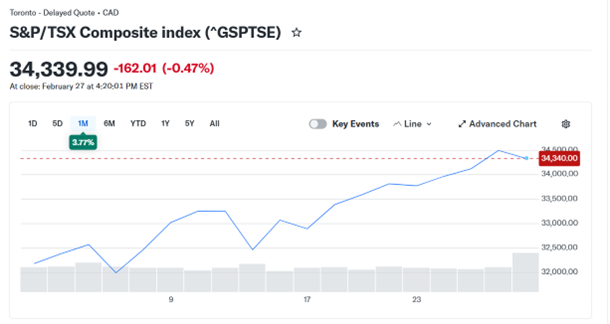

Canadian Equities:

Canadian equities edged lower into week-end. The S&P/TSX Composite Index closed at 34,339.99, declining 162.01 points (-0.47%) on Friday. The pullback followed broader global equity weakness and reflected cautious positioning into month-end.

Source: Yahoo Finance

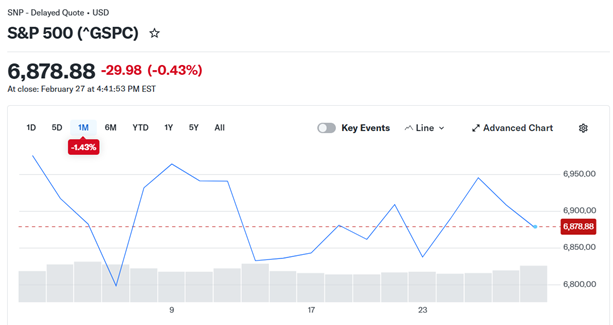

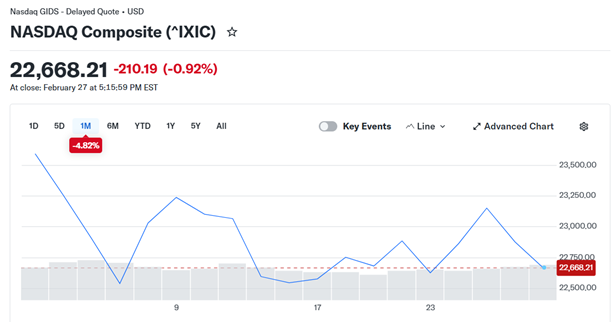

U.S. Equities:

Last week, U.S. equity markets closed lower, with technology stocks underperforming. The S&P 500 closed at 6,878.88, down 29.98 points (-0.43%) on Friday. The Dow Jones Industrial Average ended at 48,977.92, falling 521.28 points (-1.05%). The Nasdaq Composite closed at 22,668.21, declining 210.19 points (-0.92%), reflecting continued volatility in large-cap technology and AI-related names.

Source: Yahoo Finance

U.S. Bonds:

U.S. Treasury yields moved lower into the end of the week. The 10-year U.S. Treasury yield closed at 3.962%, down 5.5 basis points (-1.37%) on Friday.

Source: Yahoo Finance

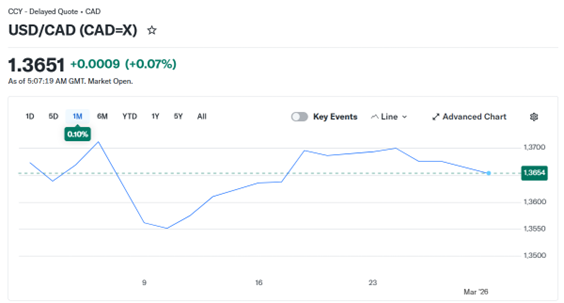

Forex Market:

The U.S. dollar remained relatively stable. The USD/CAD exchange rate closed at 1.3676, reflecting limited currency volatility amid broader market fluctuations.

Source: Yahoo Finance

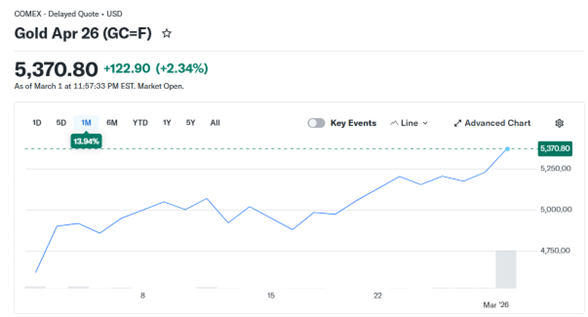

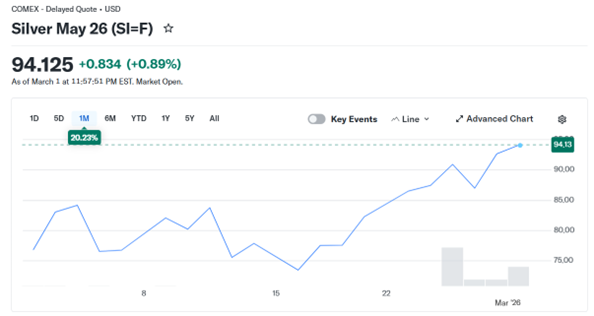

Gold Market& Silver Market:

Gold prices remained elevated. Gold futures (GC=F) closed at $5,230.50 per ounce, maintaining strength amid ongoing market volatility. Silver futures (SI=F) ended at $92.682 per ounce.

Source: Yahoo Finance

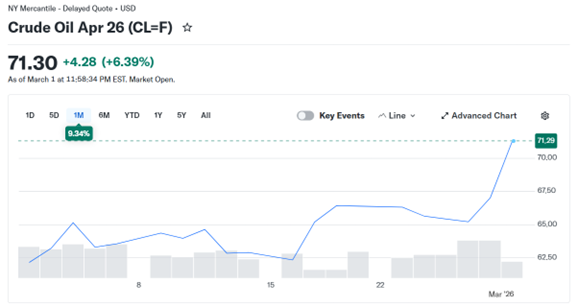

Oil Market:

Oil prices closed the week higher. WTI crude oil (CL=F) finished at $67.02 per barrel, supported by commodity strength despite equity market weakness.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of March 2 , 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

March 2 (Monday)

- Economic Data & Events: U.S. Manufacturing PMI (Feb)

- Key Earnings: Berkshire Hathaway, CrowdStrick

March 3 (Tuesday)

- Economic Data & Events: Euro Zone CPI (Feb), China Manufacturing PMI (Feb)

- Key Earnings: Target, Best Buy, GitLab

March 4 (Wednesday)

- Economic Data & Events: U.S. Services PMI (Feb), ISM Non-Manufacturing PMI (Feb)

- Key Earnings: Broadcom, Okta, American Eagle Outfitters

March 5 (Thursday)

- Economic Data & Events: Initial Jobless Claims (Feb 28)

- Key Earnings: Costco, JD, Marvell Technology, Kroger, Petrobras

March 6 (Friday)

- Economic Data & Events: U.S. Employment Report (Feb), U.S. Retail Sales (Jan)

Author by: Sarah San

Edited & Published by: Sarah San

March 2 , 2026 13:00 AM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.