Key Focus This Week:

“U.S. Inflation, Consumer Spending, Central Bank Signals and Q2 Earnings Season to Drive Market Direction”

In the United States, investors will first focus on the release of the Consumer Price Index (CPI) and Producer Price Index (PPI) to assess whether recent increases in energy and import costs are beginning to broaden into underlying goods and services inflation. Should inflation remain persistent, markets may further scale back expectations for policy easing. Conversely, signs of moderating price pressures could ease upward pressure on Treasury yields and provide support for growth-oriented equities.

Beyond inflation, this week’s U.S. Retail Sales report will offer another important gauge of consumer resilience. Investors will evaluate whether household spending continues to support economic growth or whether elevated prices, higher energy costs and tighter financial conditions are increasingly weighing on consumers. Continued strength in retail activity would reinforce confidence in the U.S. economic outlook, while a meaningful slowdown could revive concerns surrounding corporate earnings and broader economic growth.

Federal Reserve Chair Jerome Powell is also scheduled to testify before both the House of Representatives and the Senate as part of the Federal Reserve’s Semiannual Monetary Policy Report. Market participants will closely monitor his assessment of inflation, labour market conditions and the future path of monetary policy. Against the backdrop of renewed volatility in energy markets and geopolitical tensions, Powell’s remarks could become one of the week’s most influential catalysts for the U.S. dollar, Treasury yields and technology stocks.

In Canada, the Bank of Canada is widely expected to announce its latest interest rate decision while simultaneously releasing its updated Monetary Policy Report (MPR). With the Canadian economy facing improving domestic growth, ongoing trade uncertainty and fluctuating energy prices, policymakers continue to balance supporting economic activity with preventing inflationary pressures from becoming entrenched.

More importantly than the rate decision itself, investors will focus on the Bank’s updated economic projections and policy guidance. Its outlook for growth, inflation and external risks is expected to influence expectations for future interest rate decisions, while potentially driving volatility across Canadian government bond yields, the Canadian dollar, bank stocks and interest rate-sensitive sectors such as real estate.

Meanwhile, the U.S. second-quarter earnings season officially accelerates this week. Major U.S. banks will report first, providing valuable insight into loan demand, consumer credit quality, net interest income, capital markets activity and corporate financing conditions. Investors are likely to place greater emphasis on management commentary regarding credit quality and the broader economic outlook than on the quarterly results themselves.

Outside the financial sector, several key companies across the semiconductor, healthcare and streaming industries will also report earnings. Results and guidance from ASML and Taiwan Semiconductor Manufacturing Company (TSMC)will help investors evaluate whether demand for artificial intelligence infrastructure, data centres and advanced semiconductor manufacturing remains robust. Netflix will offer insight into consumer subscription spending and content monetization trends, while UnitedHealth Group may provide updated signals regarding healthcare costs and insurance industry fundamentals.

At the same time, renewed military clashes between the United States and Iran have intensified concerns surrounding control of the Strait of Hormuz, maritime security and global energy transportation. Markets will closely monitor whether tensions continue to escalate and whether crude oil shipments experience further disruption.

Should geopolitical risks intensify further, higher oil prices could reignite inflation expectations and reduce market confidence in future monetary policy easing. For Canada, rising energy prices may provide additional support for energy and resource equities, while simultaneously increasing domestic inflationary pressures and weighing on interest rate-sensitive industries and consumer-related businesses.

Week’s Key Economic Data & News Recap

Last week’s release of the Federal Reserve’s June FOMC Meeting Minutes showed unanimous support among policymakers for keeping interest rates unchanged at the June meeting. Officials generally agreed that the U.S. economy continues to expand at a solid pace, labour market conditions remain broadly healthy, while inflation remains well above the Federal Reserve’s long-term target and upside risks to price stability persist.

The minutes also revealed ongoing differences regarding the degree of policy restrictiveness and the future path of interest rates. A small number of participants suggested that rising inflation pressures could eventually justify additional policy tightening, while others argued that current interest rates have yet to become meaningfully restrictive. Higher energy costs, tariffs, supply chain disruptions and continued AI-related investment demand were all identified as factors that could sustain inflationary pressures.

Overall, the minutes reinforced expectations that the Federal Reserve will maintain a cautious policy stance in the near term. Market attention has gradually shifted from the timing of future rate cuts toward whether persistent inflation could ultimately require interest rates to remain elevated for longer—or even prompt renewed policy tightening.

Canadian Business Confidence Softens While Labour Market Remains Resilient

The Bank of Canada’s Business Outlook Survey for the second quarter indicated that business sentiment weakened after improving over the previous three consecutive quarters. Sales expectations moderated, hiring intentions fell below historical averages, and an increasing number of businesses cited elevated fuel costs and geopolitical uncertainty in the Middle East as factors weighing on domestic demand.

Business pricing expectations continued to diverge from overall operating conditions. Higher energy and input costs have pushed inflation expectations higher, while businesses outside Canada’s Prairie provinces generally expressed more cautious views toward future sales and operating activity. In contrast, firms associated with the energy and natural resource sectors remained relatively optimistic regarding investment, sales and hiring plans.

The Bank of Canada’s Canadian Survey of Consumer Expectations also showed that short-term household inflation expectations remain elevated. Trade tensions, energy prices and fuel costs have become increasingly important concerns, while higher living costs and economic uncertainty continue to restrain household spending plans. Nevertheless, consumers reported a modest improvement in labour market conditions and somewhat lower concerns regarding unemployment.

Canada’s labour market remained broadly stable in June. Overall employment changed little, while the unemployment rate declined for a second consecutive month. Employment gains among youth and core working-age workers were partially offset by weaker employment among older workers. Accommodation and food services recorded employment growth, while manufacturing employment declined. Overall, the data suggest that Canada’s labour market continues to stabilize, although meaningful differences remain across industries and demographic groups.

Technology Leadership Continues to Support U.S. Equity Markets

Major U.S. equity indices continued to advance last week despite increasing sector divergence. The S&P 500 gained 1.2%, the Nasdaq Composite advanced 1.7%, while the Dow Jones Industrial Average declined 0.5%. Strong performance in technology and consumer discretionary stocks helped push the S&P 500 closer to its record highs.

Artificial intelligence and semiconductor companies remained the primary drivers of market performance. The strong U.S. market debut of SK Hynix further strengthened investor optimism surrounding memory chips and AI infrastructure demand. However, as valuations continue to expand, investors are becoming increasingly focused on whether corporate earnings can justify current market expectations, leaving semiconductor stocks vulnerable to elevated volatility.

With second-quarter earnings season now underway, investor attention is gradually shifting away from macroeconomic policy and AI-related narratives toward actual corporate earnings, forward guidance and consumer fundamentals. Earnings from the major U.S. banks are expected to provide the first meaningful assessment of economic activity, loan demand and credit quality.

Middle East Tensions Lift Oil Prices While Gold Faces Pressure from Higher Rate Expectations

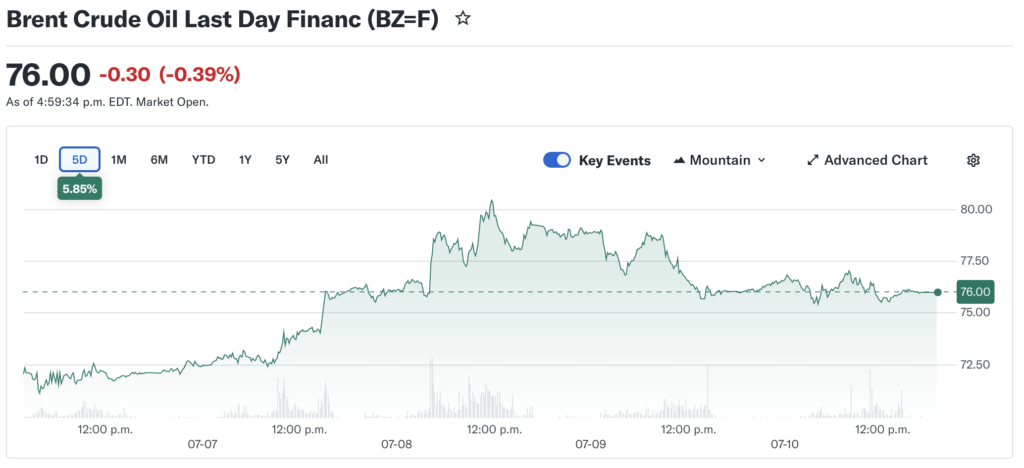

Renewed military conflict between the United States and Iran, slower shipping activity through the Strait of Hormuz and growing concerns over global crude oil supplies pushed oil prices higher last week. Although markets continue to anticipate potential de-escalation and renewed diplomatic negotiations, Brent crude gained approximately 5.5%, while WTI crude rose nearly 4% during the week.

The rebound in energy prices revived concerns regarding inflation and production costs. Higher oil prices could increase transportation and manufacturing expenses while reducing central banks’ flexibility to ease monetary policy, becoming an important driver of both bond and precious metals markets last week.

Gold, however, failed to fully benefit from increased geopolitical uncertainty. Spot gold declined approximately 1.7%over the week as rising oil prices reinforced expectations for persistent inflation and tighter monetary policy. Higher interest rate expectations increased the opportunity cost of holding non-yielding assets such as gold, offsetting part of the safe-haven demand.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index traded within a range of approximately 34,640.00 to 35,350.00, gaining approximately 0.16% over the five-day period to close at 35,305.31 on July 10. The index edged lower early in the week, briefly falling below the 34,700 level during intraday trading on July 8, before rebounding sharply on the back of strength in the energy, financial and materials sectors to reclaim the 35,000 mark. The market continued to trend modestly higher on July 9 and 10, ultimately closing near the upper end of its weekly trading range, reflecting an improvement in investor risk sentiment while remaining within a broader high-level consolidation pattern.

Source: Yahoo Finance

U.S. Equities:

Last week, the three major U.S. equity indices delivered mixed performances but generally maintained an upward trading trend. The S&P 500 Index traded within a range of 7,425.00 to 7,580.00, gaining 1.23% over the five-day period to close at 7,575.39. The NASDAQ Composite Index traded between 25,540.00 and 26,290.00, advancing 1.74% to finish at 26,281.61, reaching another record high as continued strength in mega-cap technology stocks and the semiconductor sector supported market sentiment. In contrast, the Dow Jones Industrial Average traded within a range of 52,080.00 to 53,180.00, declining 0.50% over the week to close at 52,637.01.

Source: Yahoo Finance

U.S. Bonds:

Last week, the U.S. 10-Year Treasury yield traded within a range of approximately 4.48% to 4.60%, rising 1.87% over the five-day period to close at 4.569%. The yield climbed above 4.59% early in the week, supported by stronger-than-expected economic data and expectations that the Federal Reserve would keep interest rates elevated for longer, before partially retreating. However, as investors reassessed the outlook for inflation and the timing of potential rate cuts, the 10-year yield moved back above 4.56% on Friday.

Source: Yahoo Finance

Forex Market:

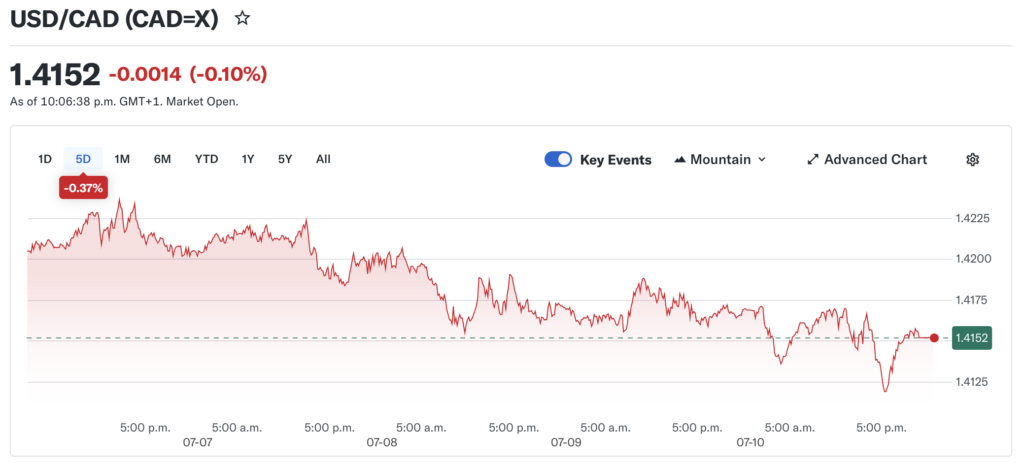

Last week, the USD/CAD exchange rate traded within a range of approximately 1.4120 to 1.4225, declining 0.35% over the five-day period to close at 1.4162. The currency pair briefly moved toward the 1.4220 level early in the week before reversing lower as stronger-than-expected Canadian employment data, an improvement in market risk sentiment and a moderation in U.S. dollar strength supported the Canadian dollar. As a result, USD/CAD retreated toward the 1.41 level.

Source: Yahoo Finance

Gold & Silver Market:

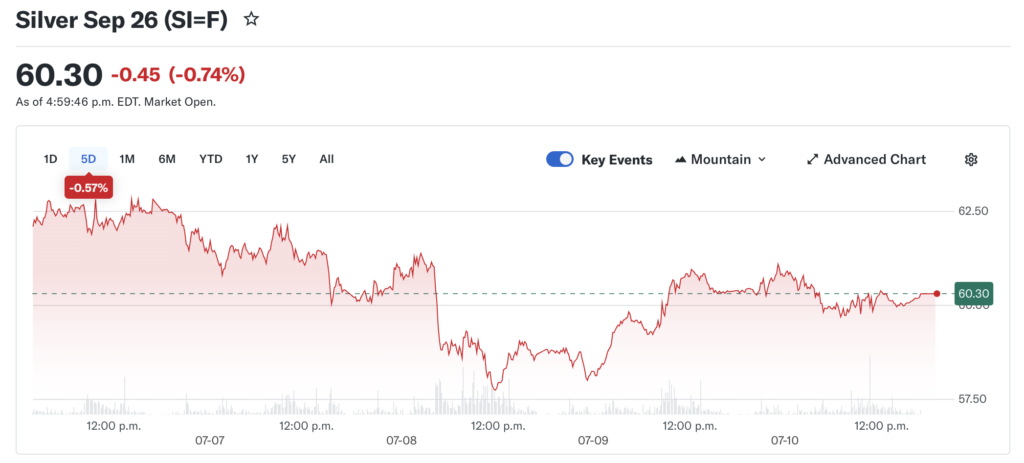

Last week, Gold Futures traded within a range of approximately 4,040.00 to 4,145.00, declining 2.03% over the five-day period to close at 4,104.10. Silver Futures traded between 57.80 and 61.30, falling 5.33% over the week to close at 59.809.

Source: Yahoo Finance

Oil Market:

Last week, Brent Crude Futures traded within a range of approximately US$75.40 to US$79.80 per barrel, gaining 10.31% over the five-day period to close at US$76.01 per barrel.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of July 13th, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (July 13 – July 17, 2026)

Monday, July 13

- After Market Close: AeroGrow and First Business Financial Services report earnings.

- Investors will begin the week by assessing earnings from smaller-cap companies ahead of a busy week featuring major U.S. banks and leading technology firms.

Tuesday, July 14

- Before Market Open: Citigroup, Goldman Sachs, JPMorgan Chase, Bank of America, Wells Fargo, Fastenal, Ericsson, AngioDynamics and DNB Bank report earnings.

- After Market Close: AEHR Test Systems, Equity Bancshares, Phoenix Education, Kestra Medical Technologies and Loop Industries report earnings.

- The U.S. second-quarter earnings season officially shifts into high gear as the nation’s largest banks report results. Investors will focus on loan demand, net interest income (NII), capital markets and investment banking activity, as well as management commentary on the U.S. economic outlook, consumer credit quality and the interest rate environment.

Wednesday, July 15

- Before Market Open: ASML, Progressive, BlackRock, Conagra Brands, Morgan Stanley, Johnson & Johnson, Elevance Health, PNC Financial, M&T Bank and Cintas report earnings.

- After Market Close: United Airlines, J.B. Hunt, Helen of Troy, Karooooo and Great Southern Bancorp report earnings.

- Markets will closely watch ASML for updates on demand for advanced semiconductor equipment driven by artificial intelligence and next-generation chip manufacturing. Earnings from BlackRock and Morgan Stanley will provide insight into global capital flows, asset management trends and investment banking activity, while Johnson & Johnson and Elevance Health are expected to offer an updated view on healthcare demand, medical cost trends and industry fundamentals.

Thursday, July 16

- Before Market Open: UnitedHealth Group, TSMC, U.S. Bancorp, GE Aerospace, Abbott Laboratories, State Street, Citizens Financial, Horizon Aircraft, Insteel Industries and Prologis report earnings.

- After Market Close: Netflix, Alcoa, Intuitive Surgical, Cohen & Steers, First National Bank, Simmons First National, Independent Bank and Wise report earnings.

- TSMC will be one of the week’s most closely watched companies, with investors looking for updates on AI-related semiconductor demand, advanced-node production and high-performance computing (HPC) trends. Meanwhile, Netflix will provide insight into subscriber growth, advertising monetization and profitability, while UnitedHealth Group is expected to offer important signals on healthcare costs, insurance margins and the broader managed care industry.

Friday, July 17

- Before Market Open: Regions Financial, Truist Financial, Fifth Third Bancorp, Autoliv, South Plains Financial, Travelers, Sandvik, Volvo, ASSA ABLOY and SKF report earnings.

- Investors will continue monitoring earnings from U.S. regional banks for trends in loan growth, credit quality and net interest income, while results from leading European industrial and manufacturing companies will provide additional insight into global economic activity, infrastructure investment and industrial demand as another busy week of earnings draws to a close.

Author by: Sarah San

Edited & Published by: Sarah San

July 13th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.