Key Focus This Week:

“Nonfarm Payrolls, ISM Manufacturing, and Labor Market Data Take Center Stage”

This week’s market focus will center on the U.S. June Nonfarm Payrolls (NFP) report, the ISM Manufacturing PMI, and the JOLTS Job Openings data. With the U.S. Independence Day holiday falling on July 4, the June employment report will be released one day earlier on July 2. Investors will closely monitor nonfarm payroll growth, the unemployment rate, and average hourly earnings to assess whether the U.S. labor market continues to demonstrate resilience. A stronger-than-expected employment report could reinforce expectations that the Federal Reserve will maintain higher interest rates for longer, while signs of a meaningful slowdown in hiring could revive discussions surrounding potential rate cuts later this year.

On the manufacturing front, the June ISM Manufacturing PMI will be released on July 1. The index rose to 54.0 in May, its highest level since 2022, signaling continued expansion in U.S. manufacturing activity. This week’s reading will provide further insight into whether the recent improvement can be sustained amid ongoing inventory rebuilding, energy price volatility, and persistent uncertainties surrounding tariffs and global supply chains.

Investors will also focus on the May JOLTS Job Openings report, scheduled for release on June 30. Job openings increased to 7.618 million in April, well above market expectations, indicating that labor demand remained relatively strong. Together with the Nonfarm Payrolls report, the JOLTS data will offer a more comprehensive assessment of whether labor market conditions are gradually cooling.

Meanwhile, the market will continue to monitor developments in AI-related companies and the semiconductor sector. Following its earnings release last week, Micron Technology issued guidance that exceeded market expectations for both revenue and earnings, while highlighting continued strength in demand for High Bandwidth Memory (HBM) products. The results reinforced the view that AI-driven data center investment continues to support robust demand for memory chips. Investors will be watching closely to determine whether AI-related capital expenditures remain strong enough to sustain the technology sector’s leadership.

Week’s Key Economic Data & News Recap

U.S. May PCE Inflation Remained Above Target, While Core Inflation Stayed Sticky

The U.S. Personal Consumption Expenditures (PCE) Price Index increased 4.1% year-over-year in May, while Core PCE rose 3.4% year-over-year and 0.3% month-over-month. As the Federal Reserve’s preferred inflation gauge, the report indicated that inflation remains well above the Fed’s long-term 2% target. Although the recent decline in oil prices has helped ease concerns over future energy-driven inflation, core inflation continued to exhibit persistence, reinforcing expectations that the Federal Reserve may need to maintain restrictive monetary policy for an extended period.

From a market perspective, the PCE report prompted investors to reassess the outlook for interest rates. With consumer spending remaining resilient, the data suggested that the U.S. economy continues to demonstrate underlying strength, while also reducing the urgency for the Federal Reserve to pivot toward monetary easing. Employment and inflation data released in the coming weeks will remain key drivers of market expectations for future monetary policy.

Strong Micron Earnings Reinforced AI Memory Demand and Supported the Semiconductor Sector

Micron’s earnings release further strengthened investor confidence in AI-related memory demand. The company issued revenue and earnings guidance above market expectations and noted that demand for High Bandwidth Memory (HBM)products remains exceptionally strong. According to Reuters, accelerating investment in AI data centers is expected to continue driving demand for AI memory chips, highlighting the strength of the ongoing AI infrastructure investment cycle.

Micron’s results reinforced the market’s view that AI infrastructure spending remains in a sustained expansion phase. Demand for HBM, AI servers, and data center infrastructure continues to serve as a key growth driver for the semiconductor industry. However, as valuations across AI-related equities remain elevated, investors are increasingly focused on earnings execution and the return on capital expenditures rather than growth expectations alone.

Oil Prices Declined Sharply, Easing Energy Inflation Concerns

International crude oil prices declined significantly last week. Concerns over potential supply disruptions in the Middle East eased as additional oil tankers resumed transit through the Strait of Hormuz, reducing market anxiety surrounding global energy supplies and driving oil prices lower from recent highs.

The decline in oil prices has helped alleviate concerns that energy costs could continue fueling inflation. Given that energy prices have been a significant contributor to inflationary pressures in recent months, lower oil prices may reduce upward pressure on future inflation readings. Nevertheless, geopolitical risks in the Middle East remain elevated, and developments in the energy market will continue to play an important role in shaping inflation expectations and the Federal Reserve’s policy outlook.

U.S. Equities Remained Near Record Highs as the AI Theme Continued to Support Risk Appetite

U.S. equities remained close to record highs last week, with AI-related sectors continuing to dominate investor attention. Although the PCE inflation report reinforced a cautious outlook for interest rates, Micron’s strong earnings reaffirmed robust demand for AI infrastructure, helping maintain positive sentiment toward technology and semiconductor stocks.

Overall, the market continues to balance persistent inflationary pressures against strong AI-driven earnings expectations. While the PCE report suggested that inflation remains above the Federal Reserve’s target, creating continued uncertainty around the interest rate outlook, corporate earnings continue to demonstrate solid demand for AI-related products and services, providing meaningful support for growth-oriented sectors. This week’s Nonfarm Payrolls, ISM Manufacturing PMI, and JOLTS Job Openings reports will be key indicators in determining the market’s next direction.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index traded within a range of 34,700.00 to 35,080.00, posting a modest 5-day gain of approximately 0.03%.

Source: Yahoo Finance

U.S. Equities:

Last week, the three major U.S. equity indices delivered mixed performance. The S&P 500 Index traded within a range of 7,300.00–7,510.00, posting a 1.97% decline over the five-day period. The NASDAQ Composite Indexfluctuated between 25,000.00 and 26,500.00, recording a 4.60% weekly loss, while the Dow Jones Industrial Averagetraded in a range of 51,400.00–52,600.00 and gained 0.58% over the week.

Source: Yahoo Finance

U.S. Bonds:

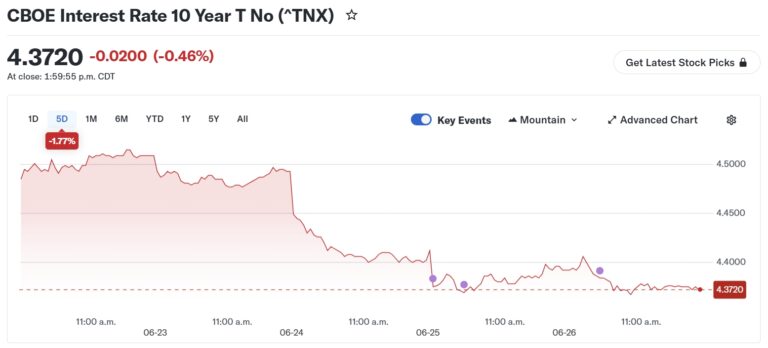

Last week, the U.S. 10-Year Treasury yield (CBOE 10-Year Treasury Note Yield Index) traded within a range of 4.37% to 4.51%, trending lower throughout the week. The yield declined 1.77% over the five-day period, closing at 4.372%.

Source: Yahoo Finance

Forex Market:

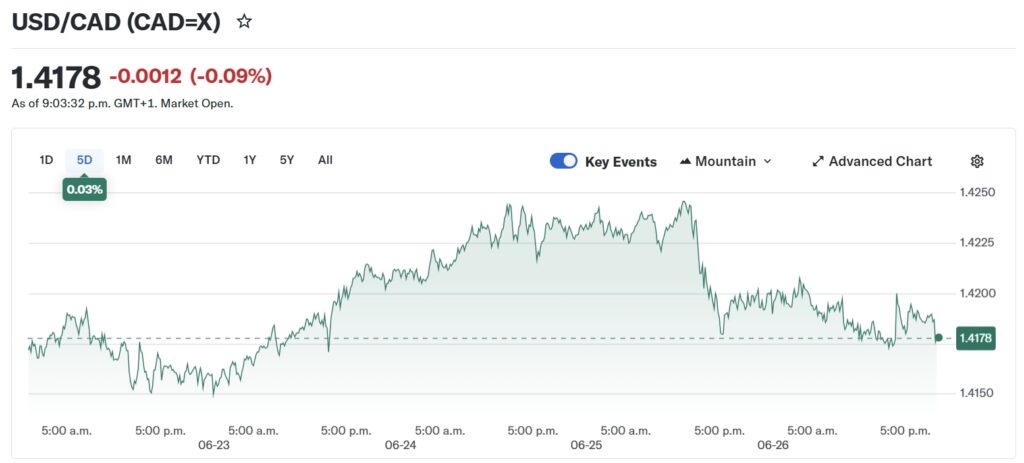

Last week, the USD/CAD exchange rate traded within a range of 1.4150 to 1.4245, moving sideways throughout the week. The currency pair posted a modest five-day gain of 0.03%, closing at 1.4178.

Source: Yahoo Finance

Gold & Silver Market:

Source: Yahoo Finance

Oil Market:

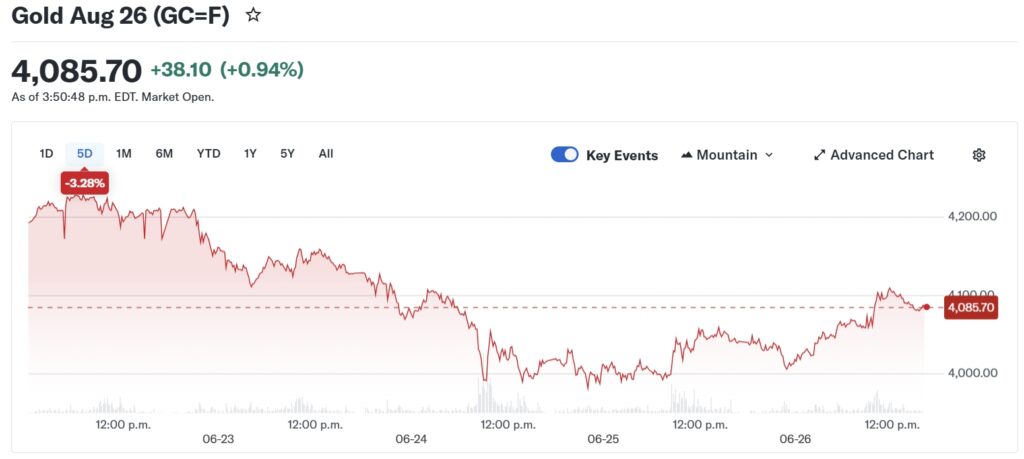

Last week, Gold Futures traded within a range of 3,980.00 to 4,220.00, trending lower throughout the week. Gold declined 3.28% over the five-day period, closing at 4,085.70. Meanwhile, Silver Futures traded between 55.80 and 66.80, posting a 10.27% weekly decline and closing at 59.48.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of June 29th, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (June 29 – July 3, 2026)

June 29 (Monday)

• AeroVironment and Concentrix are scheduled to report earnings after the market closes.

June 30 (Tuesday)

• Nike will report earnings before the market opens.

• Constellation Brands and Progress Software are scheduled to release earnings after the market closes.

July 1 (Wednesday)

• General Mills, FactSet, UniFirst, and MSC Industrial will report earnings before the market opens.

• Franklin Covey, Bassett Furniture, and Greenbrier are scheduled to report earnings after the market closes.

July 2 (Thursday)

• Lindsay Corporation will report earnings before the market opens.

July 3 (Friday)

• U.S. markets will be closed in observance of the Independence Day holiday.

Author by: Sarah San

Edited & Published by: Sarah San

June 29th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.