Key Focus This Week:

“PCE Inflation, AI Earnings and Consumer Data in the Spotlight”

This week’s market attention will center on the U.S. May Personal Consumption Expenditures (PCE) Price Index, earnings from AI-related companies, and key consumer spending data. Following last week’s Federal Reserve meeting, where policymakers left interest rates unchanged, market discussions surrounding the near-term monetary policy path have eased somewhat, with investors shifting their focus back to economic fundamentals and the inflation outlook. Against the backdrop of a resilient labor market and stronger-than-expected retail sales, this week’s economic releases and corporate earnings are expected to provide further insight into the health of the U.S. economy and the sustainability of corporate earnings growth.

On the inflation front, the U.S. Bureau of Economic Analysis (BEA) will release the May Personal Income and Outlays Report, which includes the PCE Price Index—the Federal Reserve’s preferred measure of inflation. While the recently released CPI and PPI reports indicated that inflation remains above the Fed’s long-term 2% target, the recent pullback in crude oil prices has helped ease concerns that elevated energy costs could continue to fuel inflationary pressures. As a result, whether this week’s PCE data shows further moderation in inflation will be a key driver of market expectations. A stronger-than-expected reading could reinforce concerns that interest rates may remain higher for longer, while softer inflation data would likely support risk sentiment and strengthen expectations for a more accommodative policy outlook over time.

On the corporate side, Micron Technology will report quarterly earnings this week. As one of the world’s leading memory chip manufacturers, Micron’s results are widely viewed as an important barometer for the AI investment cycle. Investors will closely monitor demand trends for data center memory, High Bandwidth Memory (HBM), and other AI-related products to assess whether AI infrastructure investment and enterprise capital expenditures remain robust. Given that artificial intelligence continues to be the dominant investment theme in equity markets, Micron’s forward guidance on AI demand and industry conditions could have a meaningful impact on the broader semiconductor sector and technology stocks.

In addition, investors will continue to monitor U.S. consumer activity. Supported by a resilient labor market and relatively stable wage growth, consumer spending remains one of the primary drivers of U.S. economic growth. Overall, this week’s PCE inflation data, AI-related corporate earnings, and consumer spending indicators are expected to be the key catalysts shaping market sentiment and providing valuable insight into the outlook for the U.S. economy and financial markets.

Week’s Key Economic Data & News Recap

Federal Reserve Holds Rates Steady as Markets Reassess the Policy Outlook

At last week’s June FOMC meeting, the Federal Reserve left the federal funds rate unchanged, in line with market expectations. However, investors focused less on the rate decision itself and more on the updated economic projections and policy signals conveyed in the Fed’s statement. Overall, policymakers acknowledged that the U.S. economy and labor market remain resilient, while inflation continues to run above the Fed’s long-term target. As a result, the Federal Reserve maintained a cautious stance regarding the future path of monetary policy.

Following the meeting, investors began to reassess expectations for future rate cuts. The Fed continues to balance the objective of bringing inflation back to target while sustaining economic growth, and upcoming inflation, employment, and consumer spending data will remain key determinants of future policy expectations. Overall, market expectations for a “higher for longer” interest rate environment have strengthened, with upcoming PCE inflation data, labor market reports, and energy price developments likely to play a critical role in shaping the Fed’s policy outlook over the coming weeks.

U.S. Retail Sales Demonstrate Continued Consumer Resilience

Data released last week by the U.S. Department of Commerce showed that retail and food services sales reached US$763.7 billion in May, increasing 0.9% month-over-month and 6.9% year-over-year. The stronger-than-expected results suggest that U.S. consumer spending remains resilient despite elevated inflation and higher energy prices.

From a sector perspective, higher gasoline prices contributed to stronger sales at service stations, although the overall improvement in retail sales extended well beyond energy-related categories. Reuters noted that May retail sales were supported by increased vehicle purchases, indicating that consumer demand has yet to show meaningful signs of slowing. Nevertheless, as elevated prices continue to weigh on household budgets, investors remain cautious about whether consumer spending momentum can be sustained. This week’s Amazon Prime Day will provide another important gauge of discretionary consumer spending trends in the U.S.

U.S. Equities Rebound as Risk Appetite Improves

U.S. equity markets rebounded last week. With U.S. stock and bond markets closed on June 19 in observance of Juneteenth, investors primarily referenced June 18 closing prices for weekly performance. Improved market sentiment followed the Federal Reserve’s decision to leave interest rates unchanged and easing concerns surrounding geopolitical tensions in the Middle East, helping support gains across the major equity indices.

Artificial intelligence remained the dominant investment theme. Although the Fed’s cautious policy stance and higher interest rates continue to pressure certain high-valuation growth stocks, investors remain optimistic about the earnings outlook for leading technology companies and the long-term growth potential of AI, providing continued support for U.S. equities.

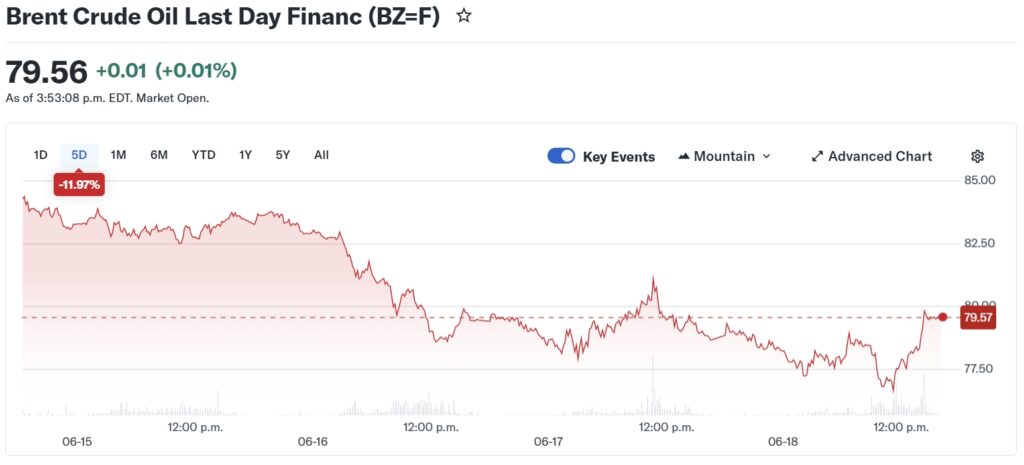

Oil Prices Decline Sharply, Easing Inflation Concerns

International crude oil prices fell significantly last week. According to Reuters, Brent crude declined by nearly 8% for the week, marking one of its largest weekly declines in recent months. The sharp pullback in oil prices has helped ease concerns that higher energy costs could reignite inflationary pressures, potentially reducing upward pressure on future inflation readings.

Nevertheless, geopolitical uncertainty in the Middle East remains elevated, and energy prices are expected to remain an important variable influencing inflation expectations and the Federal Reserve’s future policy decisions.

AI Remains the Market’s Core Theme as Micron Earnings Become the Next Key Test

Investor attention remained focused on whether the AI capital expenditure cycle can continue to support technology sector growth. Reuters noted that Micron Technology’s earnings release this week will serve as an important test of the AI investment theme, with investors closely monitoring memory chip demand, High Bandwidth Memory (HBM) orders, and management’s forward guidance to assess whether AI infrastructure investment remains robust.

While capital expenditures by major technology companies are expected to remain elevated this year, investors are placing increasing emphasis on earnings execution rather than growth narratives alone. In a higher interest rate environment, long-term AI optimism is no longer sufficient to justify premium valuations. The market will increasingly focus on whether AI investments can translate into sustainable revenue growth and margin expansion, making corporate earnings execution a key driver of future performance across the technology sector.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index traded within a range of 34,739.70 to 35,629.89, posting a weekly gain of 0.86%. Overall, Canadian equities extended their upward momentum, supported by solid performance in the energy and financial sectors, easing concerns over geopolitical tensions in the Middle East, and improving investor risk sentiment. Although the index retreated from its intraweek highs due to profit-taking and a pullback in crude oil prices, strength in heavyweight sectors continued to provide support. As a result, the S&P/TSX Composite Index recorded its third consecutive weekly advance, reflecting the resilience of the Canadian equity market despite ongoing global macroeconomic uncertainty.

Source: Yahoo Finance

U.S. Equities:

Last week, the three major U.S. equity indices moved higher amid choppy trading conditions. The S&P 500 Index traded within a range of 7,400.00 to 7,568.00, posting a 1.44% weekly gain. The NASDAQ Composite Index traded between 25,760.00 and 26,740.00, advancing 2.74% over the week, while the Dow Jones Industrial Average fluctuated within a range of 50,800.00 to 52,250.00, finishing the week 1.41% higher.

Source: Yahoo Finance

U.S. Bonds:

Last week, the U.S. 10-Year Treasury yield (CBOE 10-Year Treasury Note Yield Index) traded within a range of 4.42% to 4.50%, declining 0.27% over the five trading days to close at 4.451%.

Source: Yahoo Finance

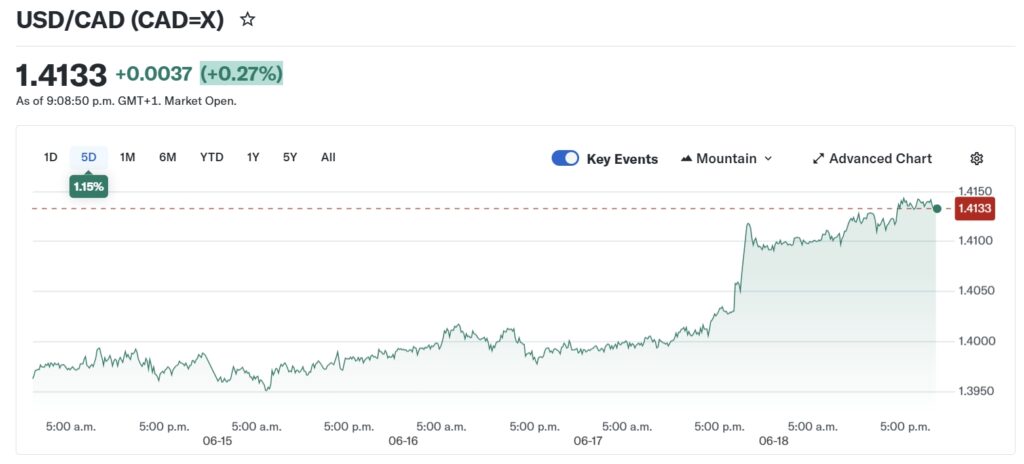

Forex Market:

Last week, the USD/CAD exchange rate traded within a range of 1.3950 to 1.4150, trending higher throughout the week. The currency pair gained 1.15% over the five trading days, closing at 1.4133.

Source: Yahoo Finance

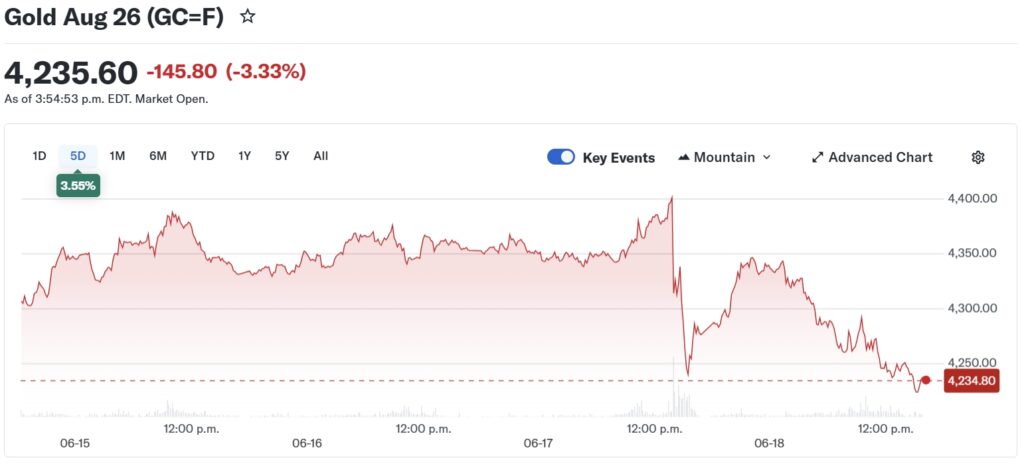

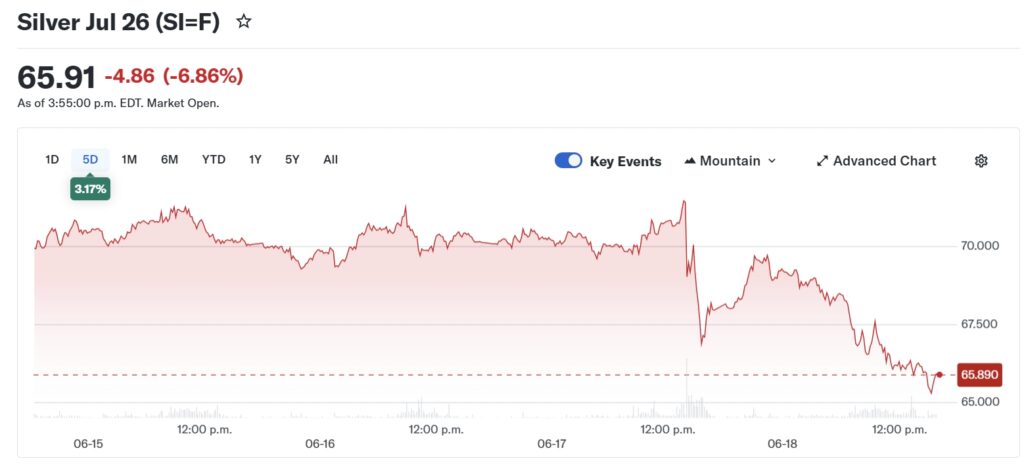

Gold & Silver Market:

Source: Yahoo Finance

Oil Market:

Last week, Brent Crude Oil Futures traded within a range of US$76.80 to US$84.50 per barrel, moving lower throughout the week. Brent crude declined 11.97% over the five trading days to close at US$79.57 per barrel.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of June 22nd, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (June 22 – June 26, 2026)

June 22 (Monday)

• Fervo Energy and Outdoor Holding Company are scheduled to report earnings before the market opens.

June 23 (Tuesday)

• Carnival Corporation, Korn Ferry, Ashtead Group (Sunbelt Rentals), and Worthington Enterprises are scheduled to report earnings before the market opens.

• FedEx, KB Home, and Cerbras Systems are scheduled to report earnings after the market closes.

June 24 (Wednesday)

• Paychex, NovaGold, Daktronics, LiveOne, and MoneyHero are scheduled to report earnings.

• Micron Technology, Trip.com Group, H.B. Fuller, Methode Electronics, MillerKnoll, and Jefferies Financial Group are scheduled to report earnings after the market closes.

June 25 (Thursday)

• Lotus Technology, Nano-X Imaging, BlackBerry, CMC, McCormick & Company, TD SYNNEX, Darden Restaurants, Virtu Financial, and Winnebago Industries are scheduled to report earnings.

• 7WISE (Seven & i-related business), American Greetings, and FedEx Freight are scheduled to report earnings after the market closes.

June 26 (Friday)

• Apogee Enterprises is scheduled to report earnings before the market opens.

Author by: Sarah San

Edited & Published by: Sarah San

June 22nd , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.