Key Focus This Week:

“Inflation Data and Rising Oil Prices Strengthen Higher-for-Longer Rate Expectations, as Markets Focus on the Federal Reserve’s Policy Path”

This week’s market focus remains centered on inflation, interest rates, and rising energy prices. Recent U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) data both came in above prior market expectations, prompting investors to reassess the outlook for future rate cuts and the broader interest rate path. At the same time, U.S. Treasury yields have remained elevated, with markets closely watching whether a prolonged high-rate environment could further pressure consumer spending, housing activity, and corporate earnings.

From the Federal Reserve’s perspective, several Fed officials recently reiterated that inflation risks have not fully subsided. Market expectations for a “Higher for Longer” rate environment have strengthened further, and some institutions have begun pushing back forecasts for the timing of future rate cuts. As a result, the market is undergoing another repricing of the monetary policy outlook.

In the energy market, geopolitical tensions in the Middle East and risks surrounding the Strait of Hormuz continue to support higher crude oil prices. Investors remain concerned that rising energy costs could further increase corporate expenses and consumer prices, potentially prolonging the current inflationary environment. Meanwhile, markets continue to monitor future OPEC+ production policy decisions and developments in global energy supply conditions.

In equities, despite ongoing inflation and interest rate pressures, major U.S. stock indices continue to trade near record highs. Artificial intelligence (AI) and mega-cap technology stocks remain the primary drivers of market performance. Investors continue to focus on whether AI-related infrastructure spending, semiconductor demand, and data center investment can sustainably support technology sector earnings growth. This week, earnings releases from companies including NVIDIA Corporation, Walmart, Target Corporation, and Home Depot are also drawing significant attention, as investors look for additional insight into AI investment demand and the resilience of the U.S. consumer.

Week’s Key Economic Data & News Recap

Earnings Season Triggers a Broad Market Repricing

U.S. April CPI rose 3.8% year-over-year, above March’s 3.3%, while core CPI increased 2.8% year-over-year, up from the previous 2.6%. Meanwhile, U.S. April PPI rose 1.4% month-over-month, marking the largest monthly increase since March 2022 and significantly above market expectations of 0.5%. On a year-over-year basis, PPI increased 6.0%, the strongest rise since December 2022. Higher energy and transportation costs were among the key drivers behind the increase in inflationary pressures.

Markets are now closely watching whether rising producer costs will continue to pass through to consumers, as this could become a critical factor shaping the future inflation trajectory. Several institutions have already begun reassessing the timing of potential future rate cuts.

U.S. April Retail Sales Rose 0.5%, Showing Signs of Moderating Consumer Growth

U.S. April retail sales increased 0.5% month-over-month, in line with market expectations but below the revised 1.6% increase in March. Core retail sales also rose 0.5%, marking the fourth consecutive monthly increase and indicating that U.S. consumer activity remains relatively resilient.

However, markets noted that part of the increase was driven by higher energy prices, while certain discretionary spending categories have started to soften. Whether persistent inflation and elevated interest rates will eventually weaken consumer spending remains an important issue for investors to monitor.

U.S. Treasury Yields Moved Higher as Markets Repriced Interest Rate Expectations

Last week, the U.S. 2-year Treasury yield moved above 4%, while the 10-year Treasury yield climbed toward 4.6%. Meanwhile, the 30-year Treasury yield rose back above the 5% level.

The continued rise in Treasury yields has created valuation pressure for growth stocks. However, due to strong demand across the AI supply chain, major technology companies have remained relatively resilient and continue to support broader equity market performance.

Middle East Tensions and Higher Oil Prices Continued to Influence Market Sentiment

Escalating tensions in the Middle East and ongoing risks surrounding the Strait of Hormuz continued to impact global energy markets. Brent crude oil prices recently remained above US$100 per barrel, increasing concerns that higher energy prices could further intensify global inflationary pressures.

Against this backdrop, the energy sector continued to outperform, while the higher-rate environment maintained pressure on smaller-cap and growth-oriented sectors. Investors also remain focused on future OPEC+ production policies and broader developments in global energy supply chains.

AI and Mega-Cap Technology Stocks Continued to Support U.S. Equity Markets

Despite ongoing macroeconomic uncertainty, AI-related and mega-cap technology stocks continued to dominate market leadership. The S&P 500 and Nasdaq indices remained near record highs, with market capital continuing to concentrate heavily in AI and large technology companies.

Investors remain focused on AI infrastructure investment, semiconductor demand, and data center expansion, as well as the earnings outlook for major technology firms. Overall, the market currently reflects a structure characterized by “indices remaining near highs, capital continuing to concentrate in mega-cap technology stocks, while internal market breadth gradually weakens.”

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index largely traded within the 33,673.80 – 34,331.80 range. Although the energy sector continued to benefit from elevated oil prices, the broader Canadian equity market showed signs of consolidation and weakening upward momentum amid rising long-term interest rates and declining overall market risk appetite.

Source: Yahoo Finance

U.S. Equities:

Source: Yahoo Finance

U.S. Bonds:

The U.S. 10-year Treasury yield has now risen significantly toward the 4.68% level and has effectively broken above the key 4.50%–4.60% consolidation range. This suggests that markets are actively repricing the future U.S. inflation outlook and interest rate trajectory, while also reflecting increasingly stronger expectations for a “Higher for Longer” rate environment.

Source: Yahoo Finance

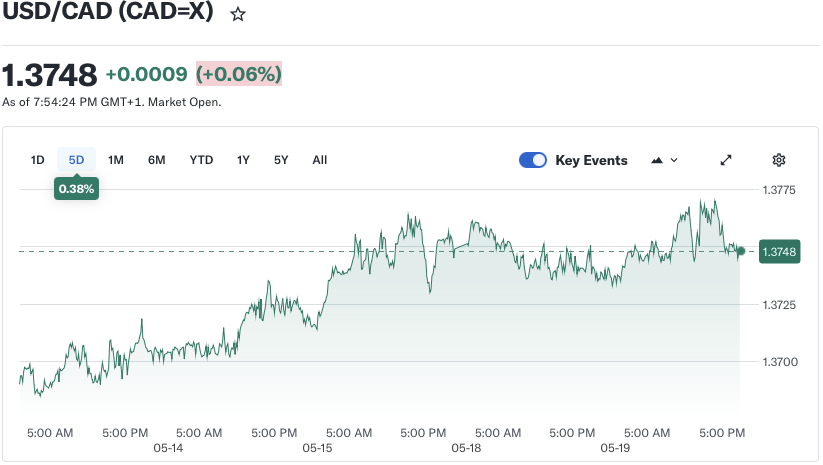

Forex Market:

From the USD/CAD price action, the exchange rate has rebounded toward the 1.3767 level and has successfully broken above the previous short-term consolidation range of approximately 1.3678–1.3766. This indicates that the U.S. dollar has regained short-term strength, while the Canadian dollar remains relatively under pressure. The broader structure reflects an “accelerating upward trend following consolidation,” suggesting markets are repricing North American interest rate differentials, oil price volatility, and changes in global risk sentiment.

Source: Yahoo Finance

Gold & Silver Market:

Based on Gold Futures price action, gold has recently declined toward the 4,490 level, with a cumulative five-day loss approaching 4%. The market currently exhibits a structure of “high-level correction followed by weak consolidation.” Prices continued to trend lower during the first half of the week and repeatedly failed to reclaim the key 4,765.20–4,524.30 resistance zone, indicating persistent selling pressure overhead.

More importantly, after U.S. Treasury yields resumed their rapid rise during the second half of the week, gold experienced another noticeable decline, highlighting that markets are once again repricing a “Higher for Longer” interest rate environment. The recent move in the U.S. 10-year Treasury yield above 4.6%, combined with continued U.S. dollar strength, has placed significant downward pressure on gold prices.

Source: Yahoo Finance

Oil Market:

Based on the performance of Brent Crude Oil Futures, the international oil market maintained an elevated and relatively firm trading structure last week. Brent crude is currently trading near the US$110 level. Although prices pulled back slightly to around US$109.26 during the final trading session of the week, the overall price base has clearly shifted higher compared to previous weeks, indicating that geopolitical risk premiums continue to dominate market pricing.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of May 19, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (May 18 – May 22, 2026)

May 18 (Monday)

- Baidu, NRX Pharmaceuticals, and Brady are scheduled to report earnings.

- Markets will focus on whether demand for AI and advertising in China continues to recover, as well as whether industrial supply chain orders are showing signs of improvement.

May 19 (Tuesday)

- Home Depot, Keysight Technologies, CAVA, and Vertiv are scheduled to release earnings.

- Home Depot will serve as a key indicator for the U.S. housing market and consumer spending trends.

- Earnings from Keysight Technologies are expected to influence market expectations surrounding semiconductor equipment demand and AI infrastructure investment.

May 20 (Wednesday)

- NVIDIA, Analog Devices, Target, Lowe’s, and TJX Companies are scheduled to report earnings.

- NVIDIA remains the market’s central focus this week, with investors closely monitoring:

- Whether AI GPU demand continues to accelerate

- Whether data center orders can sustain current growth momentum

- Whether rising AI-related capital expenditures are beginning to pressure profit margins

- If NVIDIA delivers guidance below the market’s exceptionally high expectations, the NASDAQ Composite and semiconductor sector could experience significant volatility.

May 21 (Thursday)

- Walmart, NIO, Zoom, Workday, and Ross Stores are scheduled to release earnings.

- Walmart will help determine whether U.S. consumers are increasingly shifting toward value-oriented spending behavior.

- Earnings from NIO will reflect the impact of China’s EV price competition and ongoing demand pressures.

- Workday and Zoom will provide insight into whether enterprise software spending is beginning to slow.

May 22 (Friday)

- BJ’s Wholesale Club, Deckers Brands, and Global Ship Lease are scheduled to report earnings.

- Markets will continue monitoring whether consumer demand remains resilient, while also assessing changes in transportation and logistics activity.

- If technology earnings disappoint while retail consumption continues to weaken, markets may increasingly price in a “slowing economy + higher-for-longer interest rates” scenario.

Author by: Sarah San

Edited & Published by: Sarah San

May 19th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.