Key Focus This Week:

“Market pricing is shifting from AI growth expectations toward AI earnings quality and capital efficiency”

Within this framework, the market has developed astructural bifurcation: companies with strong AI monetization capabilities (semiconductors, computing infrastructure, and cloud platforms) are characterized by revenue growth, margin expansion, and narrative validation; companies with high investment but longer payback periods typically face rising Capex, pressured FCF, and more cautious guidance; while companies with limited exposure to AI are increasingly marginalized due to a lack of earnings catalysts.

Overall, the market has shifted from anAI theme-drivenapproach to anearnings validation-drivenone. While index-level performance remains relatively stable, stock-level volatility has increased significantly due to earnings divergence. At its core, the current AI cycle is now being priced based onreturn on invested capital (ROIC)and earnings realization, with future alpha increasingly driven by a company’s ability to convert investment into cash flow and allocate capital efficiently.

Week’s Key Economic Data & News Recap

Last week, the technology sector was driven by earnings, with the key theme being the divergence in AI monetization. Companies such as Alphabet and Amazon saw strong earnings growth supported by robust cloud demand and AI-related revenues, pushing indices to new highs. In contrast, Meta Platforms and Microsoft came under pressure due to increased forward-looking capital expenditure. Overall, AI remains the dominant theme, but the market has clearly shifted from “storytelling” to “earnings validation.”

A key divergence emerged in the energy sector last week: despite elevated oil prices driven by geopolitical factors, corporate earnings did not improve in tandem. For example, Exxon Mobil and Chevron reported weaker-than-expected profits due to rising costs, inventory cycles, and pricing lags. This has led the market to reassess the investment logic of the energy sector, moving away from pure commodity price dependency toward a greater focus on cash flow stability and operational execution.

Although U.S. equity indices performed strongly last week, gains were heavily concentrated in a small number of large-cap technology companies. In particular, AI leaders such as NVIDIA contributed disproportionately to index performance, creating a divergence between index-level strength and the broader market. This “concentrated rally” masks underlying dispersion and increases market sensitivity to earnings outcomes from a few key names, amplifying downside risk if expectations are missed.

Across industrial and consumer sectors, companies generally reported stable revenue but faced margin pressure due to rising costs. Some transportation and travel companies lowered guidance due to higher energy expenses, while retailers and consumer firms relied on price increases and cost optimization to sustain profitability. In this environment, pricing power and cost control have become critical determinants of stock performance, with the market shifting its focus from top-line growth to earnings quality and operational efficiency.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Last week, the S&P/TSX Composite Index showed a pullback after a rally, declining from around 34,000 to approximately 33,700, indicating a phase of profit-taking and valuation digestion. The index remains highly sensitive to oil prices and banking sector performance due to its structural composition.

Source: Yahoo Finance

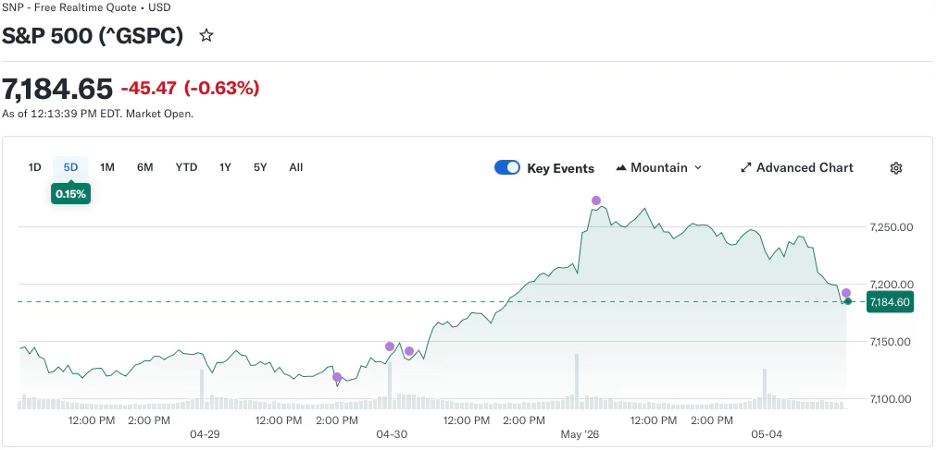

U.S. Equities:

Source: Yahoo Finance

U.S. Bonds:

The U.S. 10-year Treasury yield rose to 4.45% (+1.65%), approaching recent highs and signaling a repricing of capital costs. Rising yields create pressure on equity valuations, particularly for growth stocks, and reinforce the shift toward earnings-driven markets.

Source: Yahoo Finance

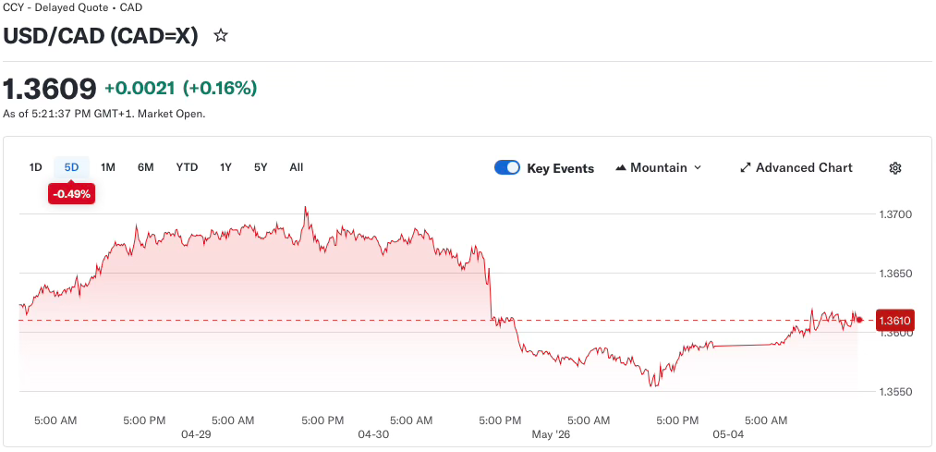

Forex Market:

USD/CAD stabilized around 1.3609, showing a rebound after a prior decline. The movement reflects a rebalancing between interest rate expectations and commodity dynamics, with oil prices supporting the Canadian dollar but momentum fading into a range-bound structure.

Source: Yahoo Finance

Gold & Silver Market:

Gold fell to 4,523 (-2.61%) and silver to 73.17 (-4.27%), both showing sharp pullbacks after recent highs. Rising real yields and a stronger dollar reduced the appeal of non-yielding assets, while profit-taking accelerated the decline.

Source: Yahoo Finance

Oil Market:

Brent crude oil rose to 113.89 (+5.29%), breaking out of its previous range and approaching recent highs. The move reflects renewed supply concerns and strong demand expectations, supporting energy markets but also contributing to inflation pressure.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of May 4, 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

Upcoming Events (May 4 – May 8, 2026)

Monday (May 4) — Industrials & Cyclicals

Tyson Foods, ON Semiconductor, and NXP Semiconductors report earnings, with focus on demand strength, cost pressures, and recovery in industrial and automotive semiconductors.

Tuesday (May 5) — AI Supply Chain Validation

Advanced Micro Devices and Super Micro Computer report, providing insight into whether AI demand is spreading beyond mega-cap leaders into the broader supply chain.

Wednesday (May 6) — Software & Data Monetization

Palantir and Datadog report, with focus on enterprise AI monetization, subscription growth, and margin expansion.

Thursday (May 7) — Platform & Consumer Tech

Uber, Airbnb, and PayPal report earnings, highlighting consumer resilience, user growth quality, and monetization efficiency.

Friday (May 8) — Market Repricing Phase

With most earnings released, markets enter a reassessment phase, focusing on capital allocation efficiency and sustainability of earnings-driven leaders.

Author by: Sarah San

Edited & Published by: Sarah San

May 4th , 2026 13:00 PM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.