Key Focus This Week: “Markets Shift to Data Watch as Rate and Inflation Uncertainty Persists”

Following last week’s central bank decisions and continued geopolitical developments, market attention this week is expected to shift toward incoming economic data for further direction. With the U.S. Federal Reserve and the Bank of Canada both maintaining a cautious policy stance, investors are now looking for confirmation on whether inflation pressures and growth trends are evolving in line with expectations.

Compared to the previous week, the macro calendar is relatively light, but several data releases will still be closely monitored. U.S. manufacturing and services PMI data will provide timely insight into business activity and demand conditions, while initial jobless claims will offer an updated view of labor market resilience. In addition, crude oil inventory data will be watched closely given the recent surge in energy prices and its implications for inflation.

Despite the quieter schedule, markets remain sensitive to developments in energy markets and geopolitical risks. Oil prices have stayed elevated near recent highs, and any further escalation or supply disruption could continue to influence inflation expectations and central bank policy outlooks. As a result, even in a lighter data week, inflation dynamics and interest rate expectations are likely to remain the dominant drivers of market sentiment.

Corporate earnings this week are relatively limited in scale, with no major large-cap releases expected. However, selected results, including from companies exposed to consumer spending and labor market conditions, may provide additional insight into the underlying strength of the economy.

Overall, markets are entering a more data-dependent phase, where incremental economic signals and external developments, particularly in energy markets, are likely to play a greater role in shaping near-term expectations.

Last Week’s Key Economic Data & News Recap

Central Bank Decisions and Rising Energy Risks Drove a More Cautious Market Tone

Central bank decisions were the main macro event last week. On March 18, the U.S. Federal Reserve kept the federal funds target range unchanged at 3.50% to 3.75%, while the Bank of Canada also left its policy rate unchanged at 2.25%. The policy decisions themselves were widely expected, but the tone was cautious. The Fed said inflation remains “somewhat elevated,” and its updated projections showed 2026 PCE inflation at 2.7%, up from 2.4% in December, while still indicating only one rate cut this year. In Canada, Governor Tiff Macklem said the Bank would be prepared to raise rates if higher energy prices risked feeding into persistent inflation.

That message pushed markets to reassess how quickly monetary policy might ease. Reuters reported that after the Fed decision, Wall Street fell and the dollar strengthened, while in Canada money markets increased their expectations for a Bank of Canada hike later this year. The shift in rate expectations also kept bond yields elevated and reinforced the market’s broader “higher-for-longer” interpretation of last week’s policy meetings.

Geopolitical Tensions and Oil Prices Kept Inflation Concerns in Focus

The other major theme was the energy shock tied to the Middle East conflict. Reuters reported that by Friday, Brent crude settled at $112.19 a barrel and front-month WTI settled at $98.32, the highest settlement levels since July 2022, as disruptions tied to the Strait of Hormuz and Iraqi force majeure declarations added to supply concerns. Because roughly 20% of global oil and LNG flows move through Hormuz, markets remained highly sensitive to each escalation in the conflict.

This mattered well beyond the energy market itself. Higher oil prices complicated the inflation outlook just as central banks were trying to judge whether price pressures were truly easing. That was especially important in Canada: February CPI slowed to 1.8% year over year, with CPI-trim and CPI-median both at 2.3%, but Reuters noted that the easing partly reflected lower gasoline prices before the full impact of the current oil shock. In other words, inflation data looked benign on the surface, but energy markets were already pointing to renewed upside risk.

Higher Yields, a Stronger U.S. Dollar, and Precious-Metal Weakness Reflected the Repricing Across Assets

Market moves across asset classes reflected that repricing. Reuters reported that hotter U.S. producer price data added to the pressure, with February PPI up 0.7% month over month and 3.4% year over year, reinforcing the Fed’s cautious stance. At the same time, weekly U.S. jobless claims fell to 205,000, signaling that the labor market remained relatively firm. Together, sticky inflation data and resilient labor conditions gave investors little reason to expect quick rate cuts.

That backdrop weighed on precious metals. Reuters reported that spot gold fell 1.8% on Friday to $4,563.64 an ounce, heading for a third straight weekly decline, while silver dropped 4.8% on the day. So gold is worth mentioning, but not as the main story by itself. Its weakness was better understood as a consequence of the week’s broader macro setup: higher yields, a stronger U.S. dollar, and reduced conviction that central banks would be able to ease policy soon. In Canada, that same mix hurt the materials sector and contributed to a 1.87% drop in the TSX on March 18, even as energy shares benefited from stronger crude prices.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

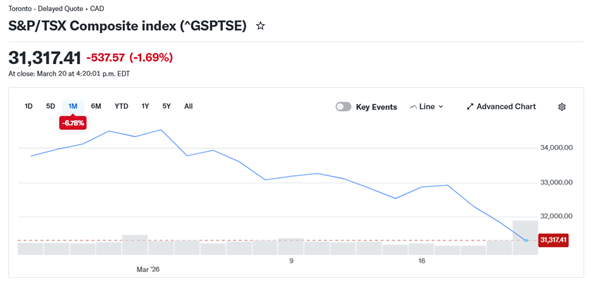

Canadian equities declined over the week, reflecting broader risk-off sentiment and weaker domestic economic conditions. The S&P/TSX Composite Index closed at 31,317.41, down 537.57 points (-1.69%) on Friday, and approximately -6.78% over the past month. While elevated oil prices provided support to the energy sector, losses in other sectors, including materials, weighed on the index.

Source: Yahoo Finance

U.S. Equities:

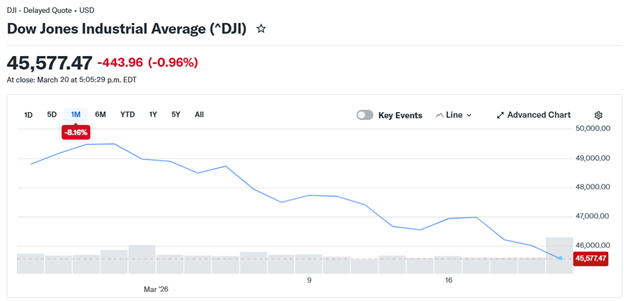

U.S. equity markets also moved lower, pressured by higher interest rates and tightening financial conditions. The S&P 500 closed at 6,506.48 (-1.51%), the Nasdaq Composite at 21,647.61 (-2.01%), and the Dow Jones Industrial Average at 45,577.47 (-0.96%). The Nasdaq underperformed, reflecting continued sensitivity of growth and technology stocks to rising yields.

Source: Yahoo Finance

U.S. Bonds:

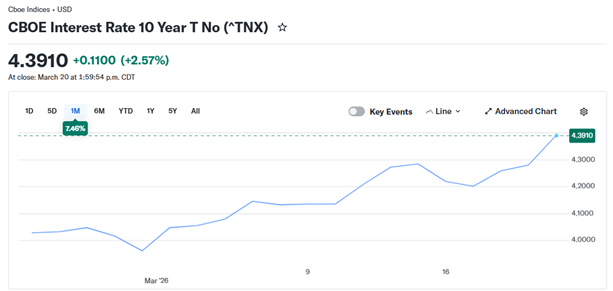

U.S. Treasury yields moved higher during the week as markets repriced interest rate expectations following central bank decisions. The 10-year U.S. Treasury yield closed at 4.391%, marking a notable increase and reaching one of its higher levels in recent months. The rise in yields contributed to downward pressure on equity valuations and precious metals.

Source: Yahoo Finance

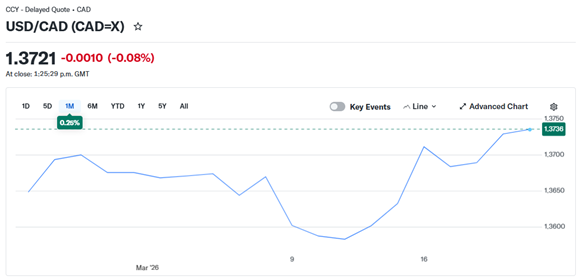

Forex Market:

In foreign exchange markets, the U.S. dollar remained strong against the Canadian dollar. The USD/CAD exchange rate closed at 1.3721, reflecting both elevated U.S. yields and relatively weaker Canadian economic data. The strength of the U.S. dollar contributed to tighter global financial conditions.

Source: Yahoo Finance

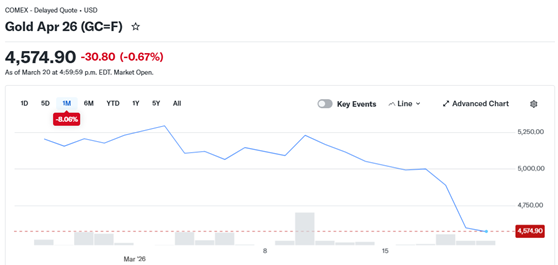

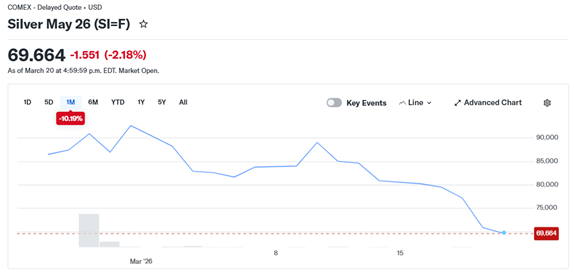

Gold Market& Silver Market:

Precious metals declined sharply during the week. Gold futures closed at $4,574.90 per ounce, down approximately 8.06% over the past month, marking one of its most significant recent pullbacks. Silver fell more sharply, with prices at $69.664 per ounce, down 2.18% on the day and over 10% on a monthly basis. The decline in precious metals was driven by rising real yields and a stronger U.S. dollar, reducing demand for non-yielding assets.

Source: Yahoo Finance

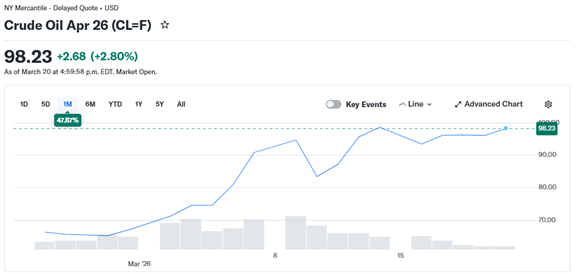

Oil Market:

Crude oil prices remained elevated amid ongoing geopolitical tensions and supply concerns. WTI crude oil closed at $98.23 per barrel, up 2.80% on the day and nearly 48% over the past month. The sustained strength in oil prices continued to support energy equities while reinforcing inflation concerns in the broader macro environment.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of March 23 , 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

March 10 (Tuesday)

- Economic Data & Events: Manufacturing PMI (Mar), Service PMI (Mar)

- Key Earnings: Braze.

March 11 (Wednesday)

- Economic Data & Events: U.S. Crude Oil Inventories.

- Key Earnings: Cintas, Paychex.

March 12 (Thursday)

- Economic Data & Events: Initial Jobless Claims.

- Key Earnings: PAVmed, Veritone.

March 13 (Friday)

- Key Earnings: Carnival Corporation.

Author by: Sarah San

Edited & Published by: Sarah San

March 23 , 2026 13:00 AM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.