Key Focus This Week “Nvidia Earnings, Inflation Data, and Policy Signals in Focus”

Following a week marked by persistent inflation readings and moderating growth signals, investor attention now turns to a critical mix of corporate earnings, fresh inflation data, and policy commentary that could shape near-term market direction.

Earnings season remains a key driver, with NVIDIA set to report on Wednesday. As a leading beneficiary of the artificial intelligence investment cycle, Nvidia’s results are expected to provide insight into the sustainability of AI-related capital spending and semiconductor demand. Given the company’s substantial weighting in major indices, its earnings could significantly influence broader equity sentiment, particularly within the technology sector. Additional reports from Salesforce, Synopsys, and Dell Technologies will further clarify trends in enterprise software, chip design, and AI infrastructure spending.

On the economic front, U.S. Producer Price Index (PPI) data for January will be released on Friday, offering another measure of upstream inflation pressures. Markets will assess whether producer prices confirm the recent persistence observed in consumer inflation data, which could influence expectations regarding the timing of potential policy adjustments by the Federal Reserve.

In Canada, fourth-quarter GDP data will be closely monitored for evidence of continued economic deceleration following softer inflation readings earlier this month. The growth data may shape expectations for future moves by the Bank of Canada, particularly if economic momentum shows further moderation.

In addition, markets will monitor remarks from U.S. President Donald Trump on Tuesday, as policy commentary may affect investor sentiment, particularly regarding fiscal priorities and trade policy direction.

With inflation signals, major technology earnings, and policy developments converging within a single week, markets may remain sensitive to data surprises and forward guidance, particularly in rate-sensitive and growth-oriented sectors.

Last Week’s Key Economic Data & News Recap

Sticky Inflation and Slowing Growth Shape Policy Outlook

U.S. inflation and growth dynamics during the week continued to signal a challenging policy environment for the Federal Reserve. The Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) Price Index, showed that inflationary pressures remained more persistent than markets had hoped. According to official data, the PCE index rose 2.9% year-over-year in December 2025, up from 2.8% in November, while core PCE (excluding food and energy) increased 3.0%, also above prior readings. The monthly pattern showed a 0.4% uptick in both headline and core inflation in December, reflecting broad price gains across services and consumer spending categories, and slightly above several economist forecasts.

This persistently elevated inflation trend, remaining above the Federal Reserve’s 2% target despite slowing headline metrics, reinforces expectations that policymakers may be reluctant to enact near-term rate cuts. At the same time, the U.S. economy’s growth trajectory moderated noticeably: the advance estimate for fourth-quarter 2025 real GDP showed annualized growth of 1.4%, down sharply from 4.4% in the prior quarter, underscoring a deceleration in economic momentum.

Taken together, these data create a complex policy picture: inflation remains sticky even as growth softens, likely tempering the pace and timing of interest rate adjustments. Markets responded to this juxtaposition with volatility in rate-sensitive assets and shifting expectations for future monetary policy.

Canadian Inflation Moderates in January

Canada’s latest inflation figures, released by Statistics Canada, indicated further moderation in consumer prices for January 2026. The headline Consumer Price Index (CPI) rose 2.3% year-over-year, down from 2.4% in December, with the deceleration largely driven by a sharper decline in gasoline prices. Excluding food and energy, CPI increased 2.4%, slightly below the prior month’s pace.

Core inflation measures, such as CPI-median and CPI-trim, commonly monitored by the Bank of Canada, also eased modestly, reinforcing indications that underlying price pressures were approaching the central bank’s target range.

While the Bank of Canada has maintained its policy rate in recent months, these softer inflation dynamics may provide additional room for policy flexibility if economic growth indicators soften further. The Canadian dollar showed modest depreciation against the U.S. dollar following the release, reflecting market reassessment of relative policy trajectories.

Supreme Court Tariff Ruling Eases Trade Uncertainty

A U.S. Supreme Court decision during the week significantly curtailed most of the prior administration’s tariff regime, effectively striking down key tariff measures that had been applied to a range of imported goods. While the ruling’s direct market impact was measured, it holds broader implications for trade policy, cost structures for importers, and inflation expectations over the medium term.

Analysts have noted that reducing tariff-related price distortions may remove an upward pressure on goods inflation that has complicated broader price stability efforts. The decision also contributes to a more predictable trade environment for multinational firms. Markets are likely to monitor subsequent tariff and trade policy developments for their influence on global supply chains, inflation, and corporate margins.

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Market Performance Review – Last Week

Source: Yahoo Finance

Canadian Equities:

Canadian equities advanced during the week, supported by strength in energy and materials. The S&P/TSX Composite Index closed at 33,817.51, gaining 222.51 points (+0.66%) on Friday. Over the past month, the index has risen approximately 2.20%, reflecting continued resilience in resource-linked sectors amid firm commodity prices.

Source: Yahoo Finance

U.S. Equities:

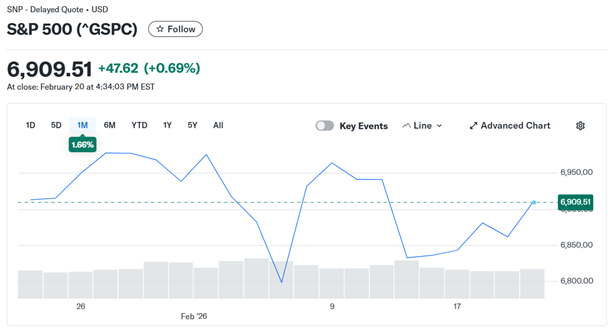

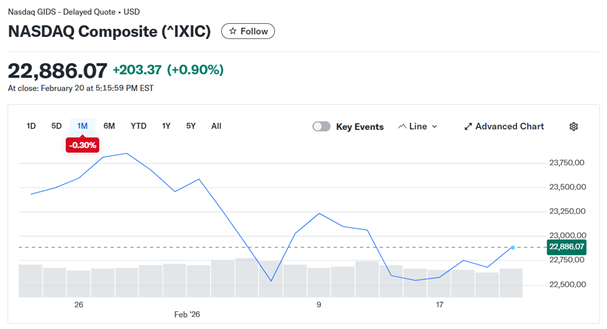

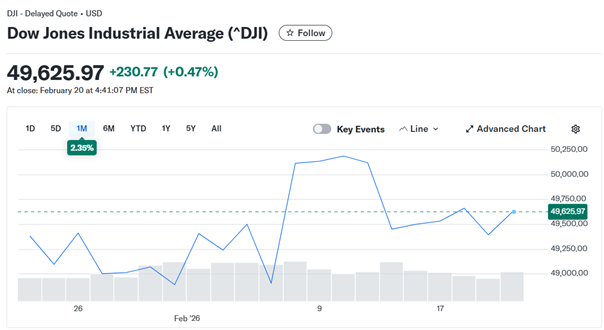

U.S. equity markets ended the week higher, with broad-based gains across major indices. The S&P 500 closed at 6,909.51, up 47.62 points (+0.69%). The Dow Jones Industrial Average finished at 49,625.97, rising 230.77 points (+0.47%). The Nasdaq Composite outperformed, closing at 22,886.07, up 203.37 points (+0.90%). Despite mid-week volatility driven by shifting rate expectations, the major indices recovered into the end of the week, suggesting continued investor participation across growth-oriented sectors.

Source: Yahoo Finance

U.S. Bonds:

U.S. Treasury yields edged higher into the close of the week. The benchmark 10-year Treasury yield closed at 4.086%, up 0.011 percentage points (+0.27%) on Friday. Over the past month, the yield remains below earlier February highs, reflecting ongoing sensitivity to inflation data and monetary policy expectations.

Source: Yahoo Finance

Forex Market:

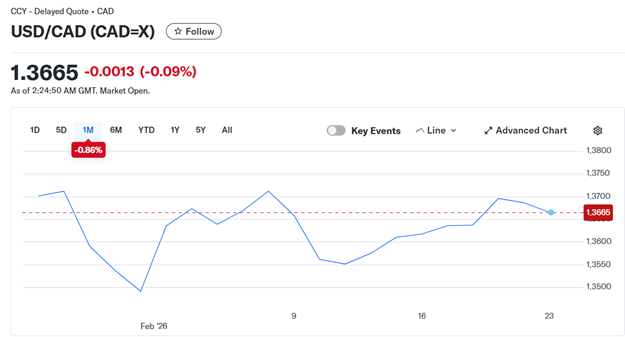

In currency markets, the U.S. dollar strengthened modestly against the Canadian dollar. USD/CAD (CAD=X) closed at 1.3687, reflecting continued divergence in monetary policy expectations between the Federal Reserve and the Bank of Canada.

Source: Yahoo Finance

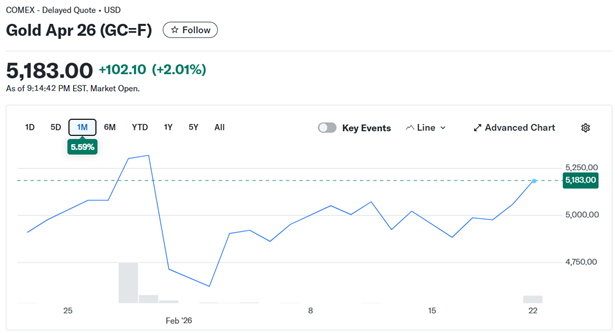

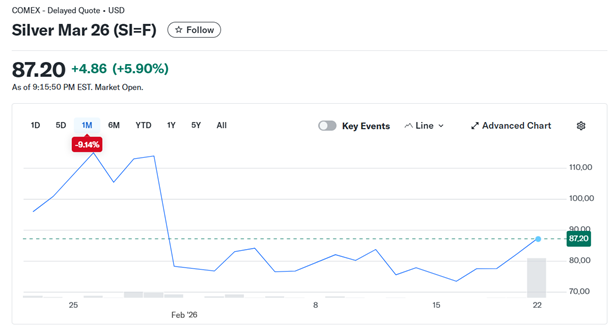

Gold Market& Silver Market:

Gold prices remained firm amid persistent inflation concerns and policy uncertainty. Gold futures closed at $5,059.30 per ounce, maintaining elevated levels as investors continued to seek inflation hedges and portfolio diversification. Silver futures ended at $82.28 per ounce, reflecting ongoing volatility within the precious metals complex.

Source: Yahoo Finance

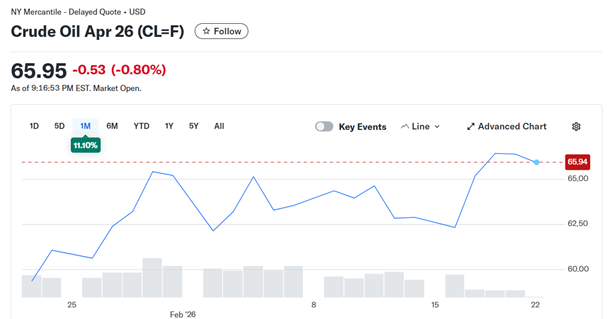

Oil Market:

WTI crude futures (CL=F) closed at $66.39 per barrel, extending gains as energy markets responded to evolving macro and geopolitical developments.

- Let us contact you

Investing with an AimStar's investment professional

Want expert advice at every step of your investing journey?

AimStar’s investment professionals can set you on the right course – and they can meet in-person or online.

Financial Market Data Copyright © 2026 AimStar myportfolio. Data as of February 23 , 2026, 12:30 PM EST

WHAT'S HAPPENING THIS WEEK

February 23 (Monday)

- Key Earnings: BWX Technologies.

February 24 (Tuesday)

- Economic Data & Events: U.S. CB Consumer Confidence (Feb), U.S. President Trump Speaks.

- Key Earnings: AMC Entertainment, MercadoLibre, Cava Group.

February 25 (Wednesday)

- Economic Data & Events: Euro Zone Core CPI (Jan), U.S. Crude Oil Inventories.

- Key Earnings: Nvidia, Salesforce, Synopsys, Bank of Montreal (BMO).

February 26 (Thursday)

- Economic Data & Events: Initial Jobless.

- Key Earnings: Dell Technologies, Baidu, Zscaler.

February 27 (Friday)

- Economic Data & Events: U.S. PPI (Jan), Canadian GDP (Q4).

- Key Earnings: Energy Fuels, Arbor Realty Trust.

Author by: Sarah San

Edited & Published by: Sarah San

February 23 , 2026 13:00 AM EST. 10 min read

AimStar Capital Group Inc. is a Canadian full-service Investment Dealer, regulated by Canadian Investment Regulatory Organization (CIRO) and a member of Canadian Investor Protection Fund (CIPF). As an independent firm, AimStar is built on a foundation of innovation, integrity, and client-centricity. They are committed to providing unbiased advice and dedicated to the client’s needs, helping them achieve their financial goals.

AimStar is recognized as a Wealth Professionals 5-star Wealth Management Firm for 2024, this award recognized AimStar has offered exceptional client experience, a proven investment track record, continuous innovation, and stringent regulatory compliance.